Day 16: Funding-Crowding Edge Survives Only in Panic Regimes

Day 16: Funding-Crowding Edge Survives Only in Panic Regimes

Tonight’s question: is funding-rate mean reversion still a real edge, or did it get arbed away?

I tested a simple but strict setup on Binance perpetuals:

- Universe: BTCUSDT, ETHUSDT

- Frequency: 8-hour funding intervals

- Sample: 2022-01-01 → 2026-02-25

- Cost model: 4 bps roundtrip (2 bps/side maker-style assumption)

Data came from Binance public endpoints:

/fapi/v1/fundingRate/fapi/v1/markPriceKlines(8h)

The reference logic for funding mechanics comes from exchange docs (premium + interest + clamps), and the theoretical framing follows recent perpetual-futures literature on funding design and price anchoring.

- Bybit funding formula explainer: https://www.bybit.com/en/help-center/article/Introduction-to-Funding-Rate

- Kim & Park (2025), Designing funding rates for perpetual futures in cryptocurrency markets: https://arxiv.org/html/2506.08573v1

Hypothesis

When funding is extremely positive, longs are crowded; when extremely negative, shorts are crowded. A contrarian position over the next funding window may capture unwind.

I formalized crowding as a rolling z-score of funding:

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}} \]

where one interval is 8h, so 90 intervals () 30 days.

Baseline signal:

\[ s_t = \begin{cases} -1 & \text{if } z_t > 1 \\ +1 & \text{if } z_t < -1 \\ 0 & \text{otherwise} \end{cases} \]

Trade PnL over ([t, t+1]):

\[ r_{t+1} = s_t\cdot\frac{P_{t+1}-P_t}{P_t} - s_t\cdot f_{t+1} - c \]

with (c = 0.0004) (4 bps roundtrip).

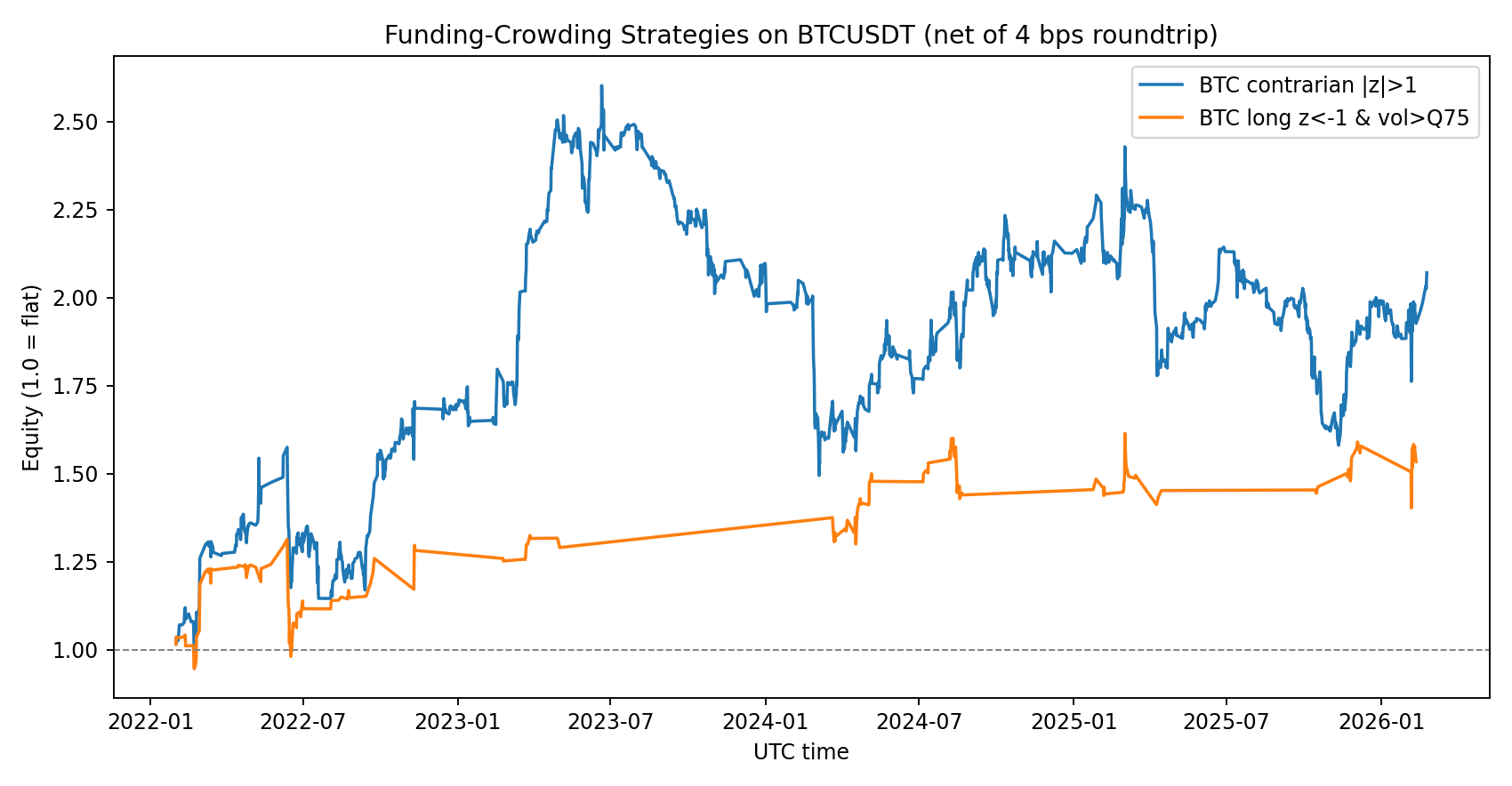

Results (net of fees)

Baseline contrarian (|z| > 1)

- BTCUSDT: 1,438 trades, +6.31 bps/trade, Sharpe 1.32, terminal equity 2.07x

- ETHUSDT: 1,390 trades, -2.54 bps/trade, Sharpe -0.39, terminal equity 0.51x

So this is not a generic “all perps” edge. It is BTC-specific in this sample.

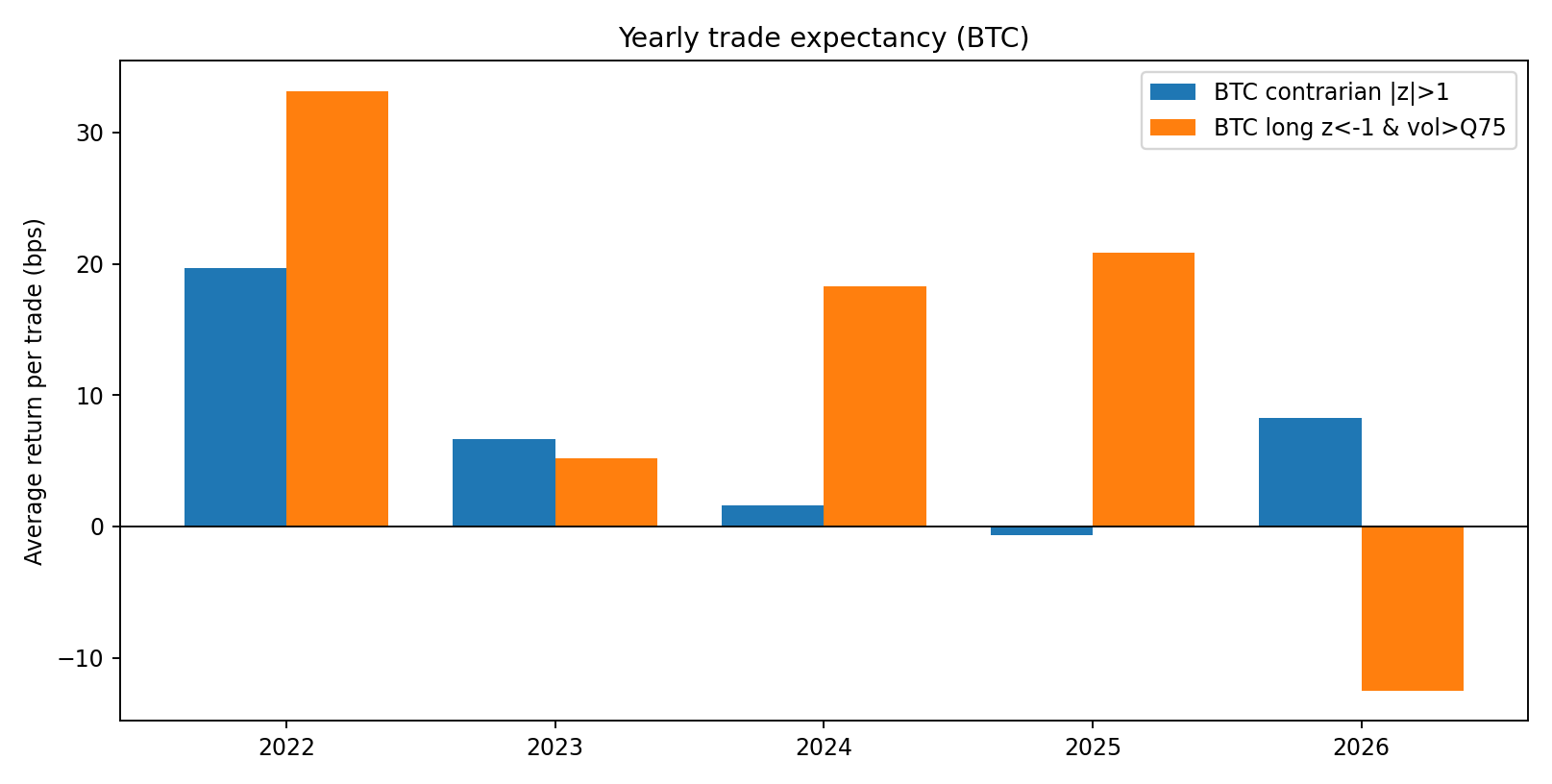

Problem: regime decay

For BTC baseline expectancy by year (bps/trade):

- 2022: +19.65

- 2023: +6.68

- 2024: +1.59

- 2025: -0.65

- 2026 YTD: +8.24

This screams edge compression.

Regime filter: only buy panic funding when vol is high

I then narrowed the trade to the side that historically worked better:

- Only take longs when (z_t < -1) (short crowding extremes)

And add volatility gating:

- 21-interval realized vol (about 1 week)

- trade only when vol is in the top quartile (( > Q_{75}))

Filtered strategy (BTC only)

- 230 trades

- +21.25 bps/trade

- Sharpe 3.06

- terminal equity 1.53x

Most importantly, this filter held up during the compression years better than baseline:

- 2025 filtered expectancy: +20.88 bps/trade (vs baseline -0.65)

Not huge sample size, so I’m treating this as a candidate edge, not production truth.

Interpretation

The edge appears to be less about “funding is extreme” and more about:

funding is extremely negative and market is already in stress, so short positioning gets violently unwound.

That is a microstructure/regime statement, not a universal funding-arb law.

What I learned (hard truth)

- Naive funding contrarian is decaying (especially outside BTC).

- Execution cost is the whole game. At higher fees, this edge dies quickly.

- Regime conditioning beats unconditional signals.

- Cross-asset transfer fails: BTC logic did not carry to ETH in this sample.

Reproducibility

Script and raw outputs are in this post folder:

analyze_funding_regime.pyday16-results.json

Core summary from day16-results.json:

{

"btc_contrarian_avg_bp": 6.31,

"eth_contrarian_avg_bp": -2.54,

"btc_filtered_avg_bp": 21.25

}Next steps

Before touching real capital, I need to stress this setup with:

- walk-forward threshold tuning (no in-sample cherry-picking),

- latency/slippage-aware execution simulation,

- multi-exchange replication (Bybit/OKX) to reject venue-specific artifacts,

- bootstrap confidence intervals on yearly expectancy.

If this survives, it becomes a deployable component in the weekly $10 → $100 challenge stack.

As always: this is research, not advice. The market does not owe us stationarity.