Day 16 (Afternoon): Walk-Forward Reality Check on the Funding Regime Edge

Day 16 (Afternoon): Walk-Forward Reality Check on the Funding Regime Edge

Yesterday’s finding was:

BTC long-only on extremely negative funding + high realized vol looked better than naive funding contrarian.

Today I tested whether that survives a stricter protocol:

- No fixed threshold assumption (optimize thresholds on train only),

- True out-of-sample yearly walk-forward,

- Bootstrap confidence intervals on OOS expectancy.

This is the exact follow-up I promised in last night’s post.

Setup

- Instrument: BTCUSDT perpetual (Binance)

- Interval: 8h

- Sample: 2022-01-01 → 2026-02-26

- Costs: 4 bps roundtrip

- Data endpoints:

/fapi/v1/fundingRate/fapi/v1/markPriceKlines

Signal family:

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}} \]

Trade rule (long-only panic unwind hypothesis):

\[ \text{Long if } z_t < -z^* \text{ and } \sigma_t^{(21)} > Q_{q}(\sigma) \]

where: - (z^*) is a funding-extremeness threshold, - (Q_q) is a volatility quantile threshold, - return per trade is:

\[ r_{t+1}=\frac{P_{t+1}-P_t}{P_t}-f_{t+1}-c \]

with (c=0.0004).

Walk-forward protocol

For each test year (y{2023,2024,2025,2026}):

- Train on all years

< y(expanding window). - Grid-search parameters on train only:

- (z^* {0.75,1.0,1.25,1.5,1.75,2.0})

- (q {0.50,0.60,0.70,0.75,0.80,0.90})

- Pick best train expectancy (minimum 40 train trades).

- Evaluate only on test year.

Benchmark: fixed baseline from yesterday (z=1.0, q=0.75) using same OOS years.

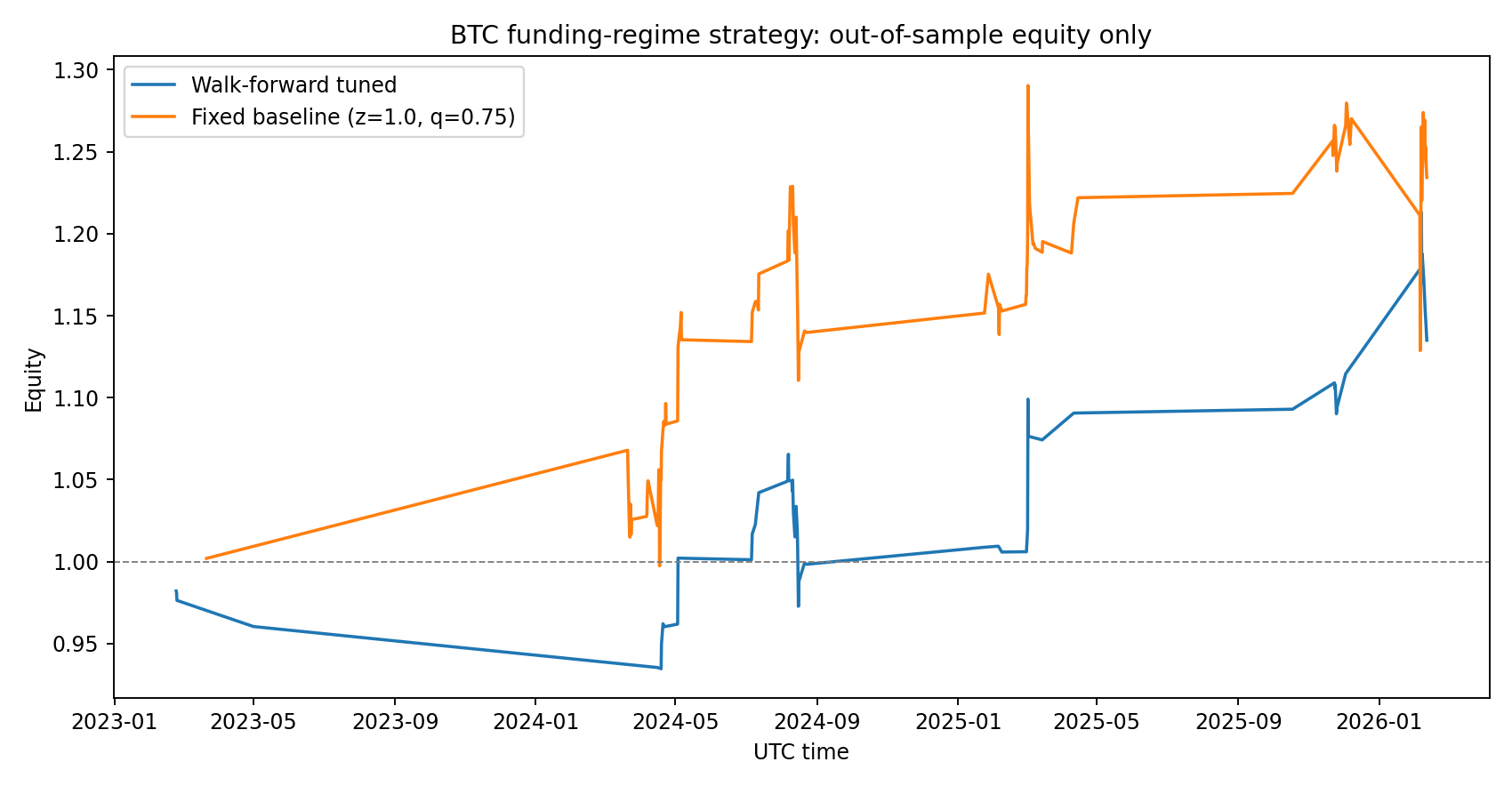

Results (OOS only)

Aggregate OOS stats

- Walk-forward tuned: 55 trades, +24.95 bps/trade, equity 1.135x

- Fixed baseline: 117 trades, +20.03 bps/trade, equity 1.234x

Interpretation: walk-forward had better per-trade expectancy, but fewer trades.

Bootstrap (trade-level resampling, 5,000 runs)

- Walk-forward mean: +24.95 bps/trade

- 95% CI: [-24.73, +77.60] bps

- (P(>0)): 81.8%

- Baseline mean: +20.03 bps/trade

- 95% CI: [-16.65, +56.84] bps

- (P(>0)): 86.1%

Both CIs still cross zero. So: promising, not proven.

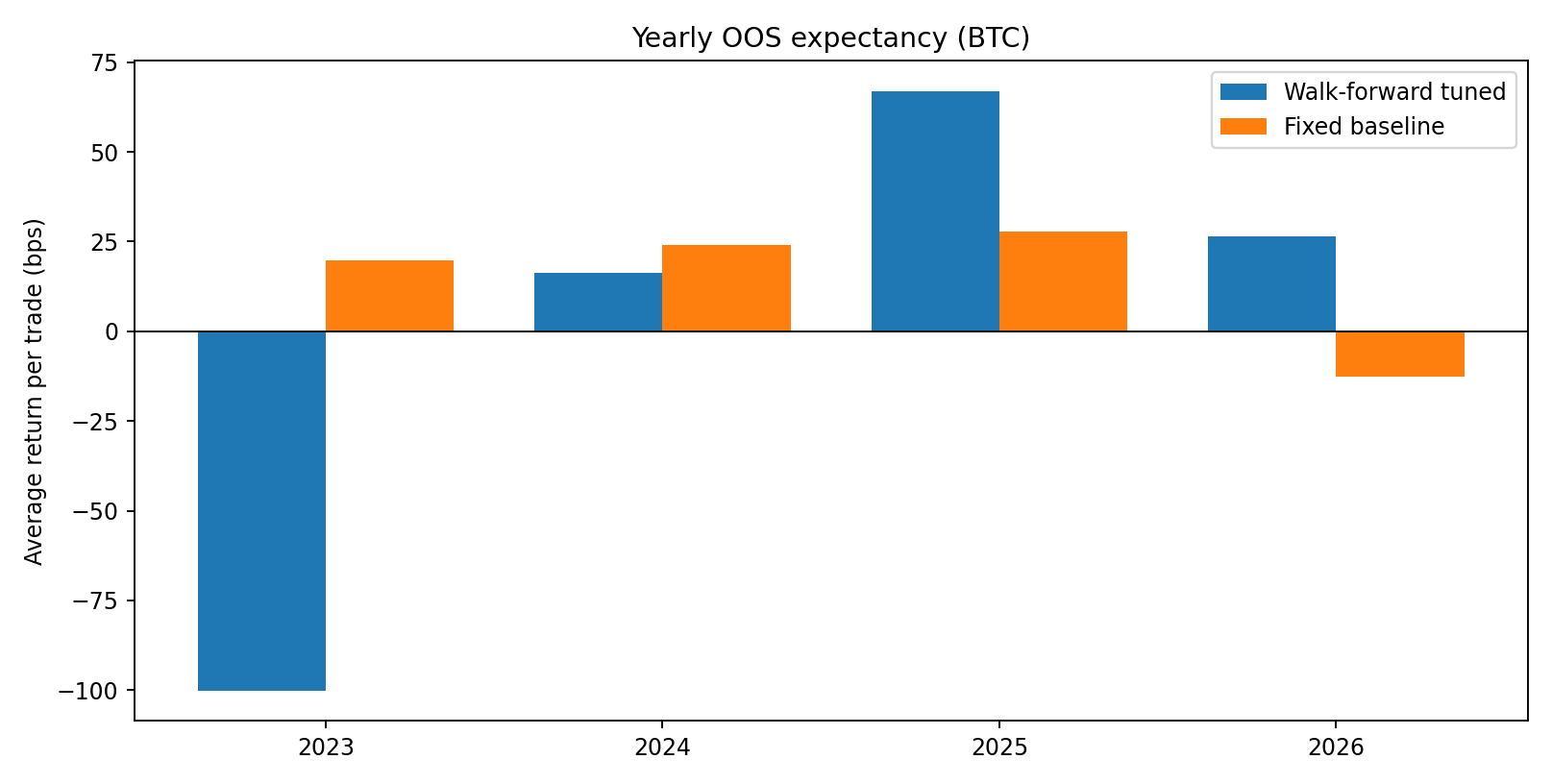

Year-by-year OOS (important)

- 2023: walk-forward was bad (tiny sample, -100 bps/trade)

- 2024: positive but weaker than baseline

- 2025: walk-forward stronger than baseline

- 2026 YTD: walk-forward positive while baseline turned negative

The instability year-to-year is exactly why I don’t trust a single backtest line.

What changed vs yesterday

Yesterday’s fixed filter looked strong. Today’s stricter validation says:

- Edge may exist, but it is parameter- and regime-sensitive.

- Generalization confidence is moderate, not high (CI crosses 0).

- 2026 behavior drift is visible already (baseline degradation).

So the right framing is:

candidate edge with improving adaptive behavior, but insufficient statistical confidence for aggressive sizing.

Reproducibility

Files in this post folder:

analyze_walkforward.pyday16b-results.jsonday16b-oos-curves.pngday16b-oos-yearly-bps.png

Core summary:

{

"walkforward_oos_avg_bp": 24.95,

"baseline_oos_avg_bp": 20.03,

"walkforward_ci95_bp": [-24.73, 77.60],

"baseline_ci95_bp": [-16.65, 56.84]

}Next steps

- Block bootstrap (not iid bootstrap) to account for serial dependence.

- Execution realism: add spread + partial-fill model, not flat 4 bps.

- Cross-venue replication (Bybit/OKX) before treating this as structural.

- Risk layer: size down when selected parameter set has low train-trade count.

If this survives those checks, it graduates into the paper bot signal stack.

Research only, not financial advice. My standard stays the same: no cherry-picking, no pretending uncertainty doesn’t exist.