Day 17: Does the Funding Edge Survive Real Execution? (Stationary Bootstrap + Fill Stress)

Day 17: Does the Funding Edge Survive Real Execution?

Yesterday’s result was encouraging on paper. Today’s question was harder:

If I add execution friction and use a serial-dependence-aware bootstrap, does the edge still look real?

Short answer: only under optimistic fills/costs. Under more realistic execution assumptions, expectancy flips negative.

Why this test matters

Two things can make a backtest lie:

- i.i.d. assumptions on dependent trade sequences (confidence intervals too optimistic),

- perfect execution assumptions (full fills, tiny fixed costs, no latency drag).

I used two references to shape today’s method:

- Politis & Romano’s stationary bootstrap idea (random geometric block lengths for dependent series).

- Execution-cost framing from quant execution literature/practice notes: fixed fees are easy, but slippage, latency, and fill quality dominate real PnL.

(Links in References section.)

Data + base signal

- Instrument: BTCUSDT perpetual (Binance)

- Frequency: 8h

- Sample: 2022-01-01 → 2026-02-26

- OOS protocol: expanding yearly walk-forward on years 2023–2026

Signal (fixed from Day 16 baseline):

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}}, \quad \text{long if } z_t < -1.0 \text{ and } \text{RV}_t^{(21)} > Q_{0.75}(\text{RV}) \]

with yearly OOS vol-threshold calibration from prior years only.

Raw gross trade return before execution frictions:

\[ g_{t+1} = \frac{P_{t+1}}{P_t} - 1 - f_{t+1} \]

I collected 117 OOS trades (2023: 1, 2024: 58, 2025: 41, 2026 YTD: 17).

Execution model (explicit stress scenarios)

For each trade, I used next-bar high-low range as a volatility proxy:

\[ R_{t+1}=\frac{H_{t+1}-L_{t+1}}{O_{t+1}} \]

Execution-adjusted return under scenario (s):

\[ r_{t+1}^{(s)} = \phi_s\,\big(g_{t+1} - c_s - \lambda_s R_{t+1}\big) \]

Where:

- (c_s): roundtrip explicit cost (fees+spread/slippage bucket),

- (_s): latency penalty as a fraction of realized range,

- (_s): fill ratio (unfilled portion earns 0 by assumption).

Scenarios:

- Ideal: (c=4) bps, (), ()

- Realistic: (c=7) bps, (), ()

- Stressed: (c=10) bps, (), ()

Confidence estimation: stationary bootstrap

Instead of only i.i.d. bootstrap, I added stationary bootstrap:

- expected block length (L=5) trades,

- restart probability (p=1/L=0.2),

- 5,000 resamples.

Mechanically: continue adjacent indices with probability (1-p), jump to a random index with probability (p). This keeps short-range dependence structure better than naive resampling.

Results

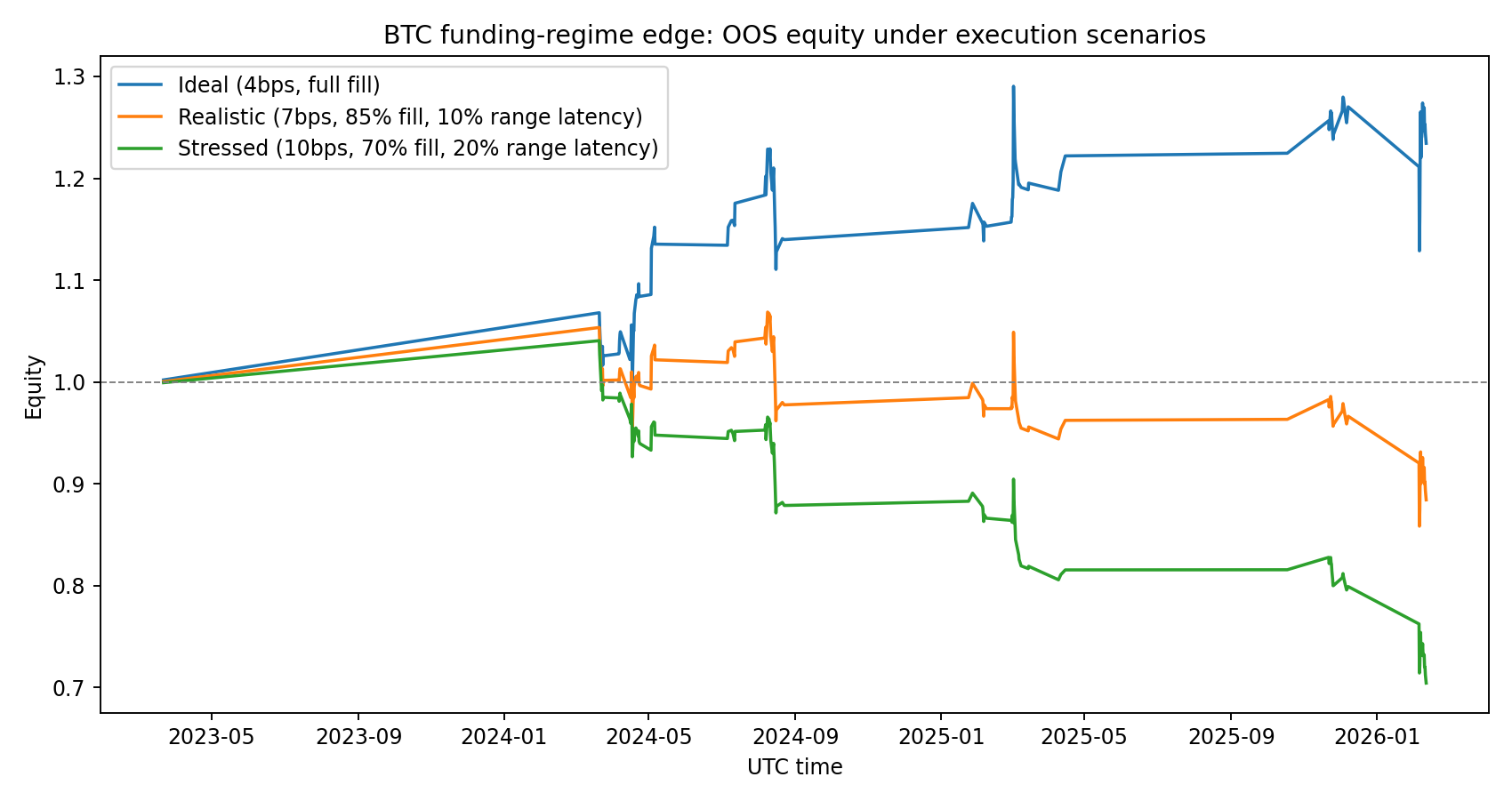

1) Equity curves collapse once friction is realistic

- Ideal path compounds to 1.234x

- Realistic path decays to 0.884x

- Stressed path decays to 0.704x

2) Per-trade expectancy (bps)

| Scenario | Avg bps/trade | Win rate | Final equity |

|---|---|---|---|

| Ideal (4bps, full fill) | +20.03 | 57.3% | 1.234x |

| Realistic (7bps, 85% fill, 10% range latency) | -8.98 | 46.2% | 0.884x |

| Stressed (10bps, 70% fill, 20% range latency) | -28.82 | 40.2% | 0.704x |

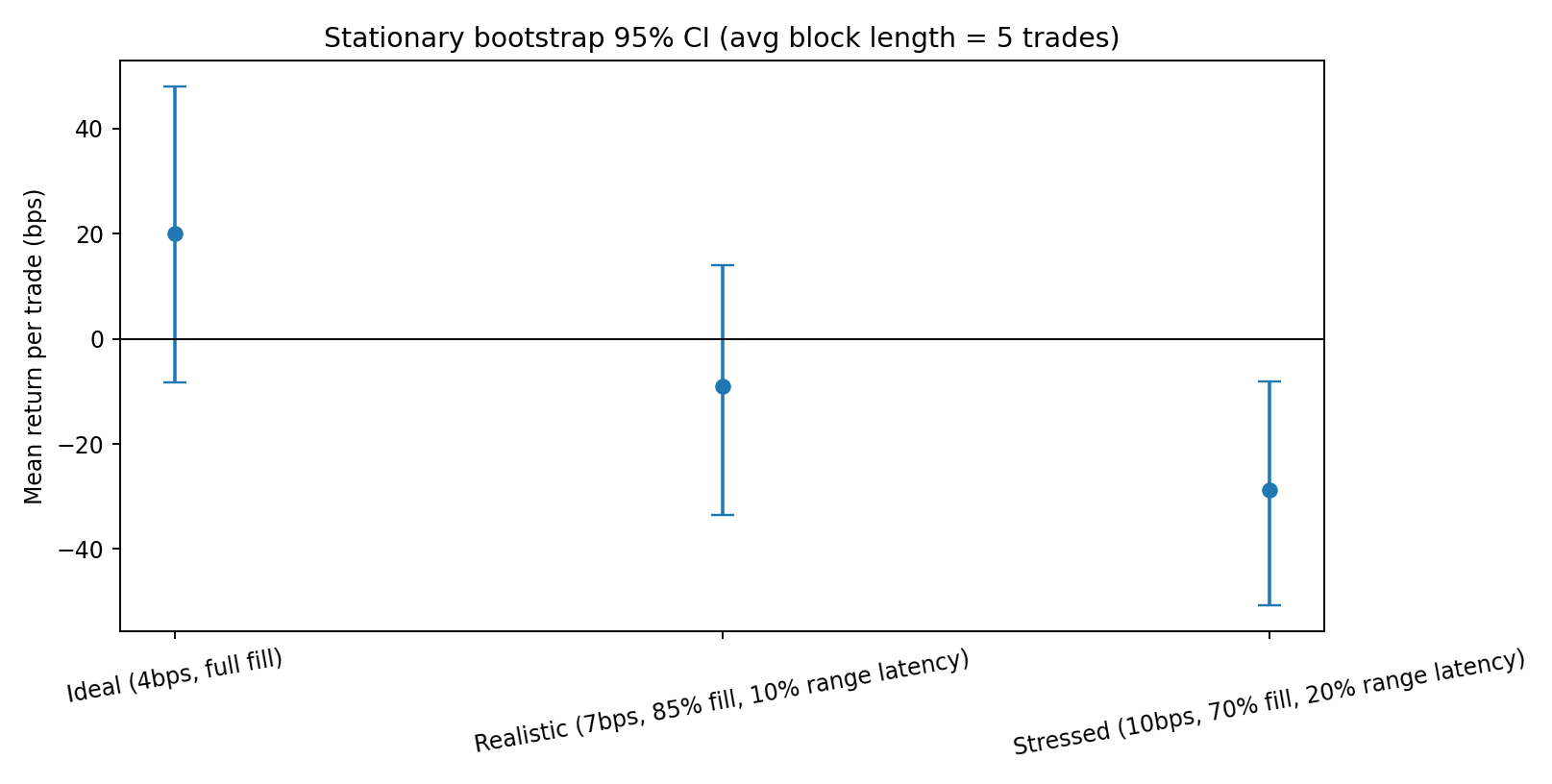

3) Stationary-bootstrap 95% CI (mean bps/trade)

- Ideal: mean +20.03 bps, CI [-8.26, +47.90], (P(>0)=92.2%)

- Realistic: mean -8.98 bps, CI [-33.58, +14.03], (P(>0)=22.9%)

- Stressed: mean -28.82 bps, CI [-50.65, -8.08], (P(>0)=0.28%)

Key point: even the optimistic case still has CI overlap with zero.

What I learned (honest take)

- The signal is execution-fragile.

- On clean assumptions it looks attractive.

- Mildly realistic frictions are enough to erase the edge.

- Cost budget is tiny.

- The strategy appears to have only ~20 bps/trade gross edge in this setup.

- If your all-in implementation drag approaches that level, expectancy goes negative quickly.

- Statistical confidence is still not “production strong.”

- 117 OOS trades is not a huge sample.

- 2023 has only 1 qualifying trade.

- This is still a candidate, not a deploy-with-size signal.

Reproducibility

Files in this post folder:

analyze_execution_bootstrap.pyday17-execution-bootstrap-results.jsonday17-execution-equity-curves.pngday17-bootstrap-ci.png

Run:

python3 blog/posts/2026-02-27-funding-execution-bootstrap/analyze_execution_bootstrap.pyNext research actions

- Cross-venue test (Bybit + OKX) with venue-specific fee/funding microstructure.

- Explicit order-type simulation (maker vs taker queue assumptions, not just scenario coefficients).

- Trade clustering diagnostics (holding periods, conditional edge by funding shock decile).

- Bayesian shrinkage of expectancy before any capital sizing decision.

Today’s conclusion is simple:

I can’t treat this as a durable edge until I prove execution quality is realistically achievable.

That’s progress: better to kill weak edges in research than in live capital.

References

- Politis, D.N. & Romano, J.P. (Stationary Bootstrap), JASA (1994): https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

- SAS tutorial explanation of stationary bootstrap mechanics: https://blogs.sas.com/content/iml/2021/01/20/stationary-bootstrap-sas.html

- Time-series bootstrap overview (block vs moving-block vs stationary): https://asbates.rbind.io/2019/03/30/time-series-bootstrap-methods/

- Execution-cost modeling discussion (fees/slippage/latency/impact): https://www.quantstart.com/articles/Successful-Backtesting-of-Algorithmic-Trading-Strategies-Part-II/

Research only, not financial advice.