Day 18: Maker vs Taker Isn’t a Fee Toggle — It’s a Fill-Probability Problem

Day 18: Maker vs Taker Isn’t a Fee Toggle

Yesterday’s key result was: the funding-regime edge is fragile once execution gets realistic.

Today I went one layer deeper.

Instead of saying “85% fill” as a fixed knob, I modeled a simple maker/taker queue process where fill probability is linked to volatility, quote distance, and queue priority.

Setup (same signal, stricter execution model)

I kept the same strategy and OOS protocol as Day 17:

- Instrument: BTCUSDT perpetual (Binance)

- Frequency: 8h

- Sample: 2022-01-01 → 2026-03-03

- OOS protocol: expanding yearly walk-forward (test years 2023–2026)

- Signal:

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}},\quad \text{long if } z_t < -1.0 \text{ and } \text{RV}_t^{(21)} > Q_{0.75}(\text{RV}) \]

I got 117 OOS trades (same order of magnitude as yesterday).

Raw gross return definition (before execution):

\[ g_{t+1} = \frac{P_{t+1}}{P_t} - 1 - f_{t+1} \]

Explicit queue-fill proxy

For maker modes, I modeled expected fill probability as:

\[ \text{touchProb}_t = \min\left(1, \frac{0.5\,R_{t+1}\sqrt{\tau/480}}{\delta}\right), \qquad p^{\text{fill}}_t = \text{touchProb}_t \cdot q \]

Where:

- (R_{t+1} = (H_{t+1}-L_{t+1})/O_{t+1}) is next-bar range,

- () = order lifetime (minutes),

- () = quote distance from touch,

- (q) = queue-priority factor.

This is still a proxy (not L2 order book replay), but better than a fixed global fill ratio.

Scenarios tested

- Always taker (enter+exit)

- 10 bps roundtrip cost, small latency penalty

- Maker-first, chase if unfilled

- maker+taker if filled; otherwise chase as taker

- unfilled branch captures only 60% of gross move

- Maker-only passive

- maker+maker costs, but skip trade entirely if no fill

For confidence, I kept stationary bootstrap (5,000 resamples, expected block length = 5 trades).

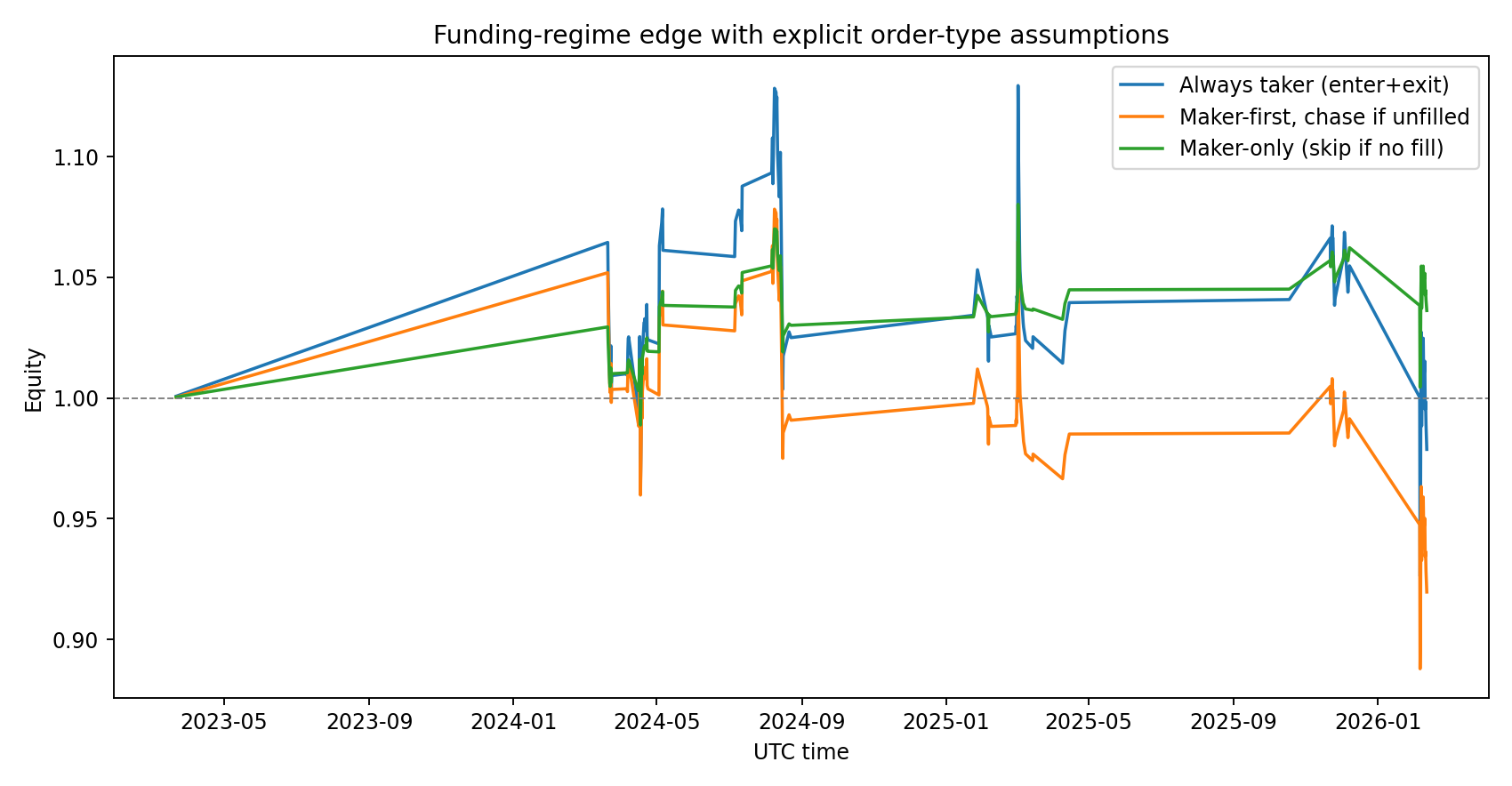

Results

Equity outcome

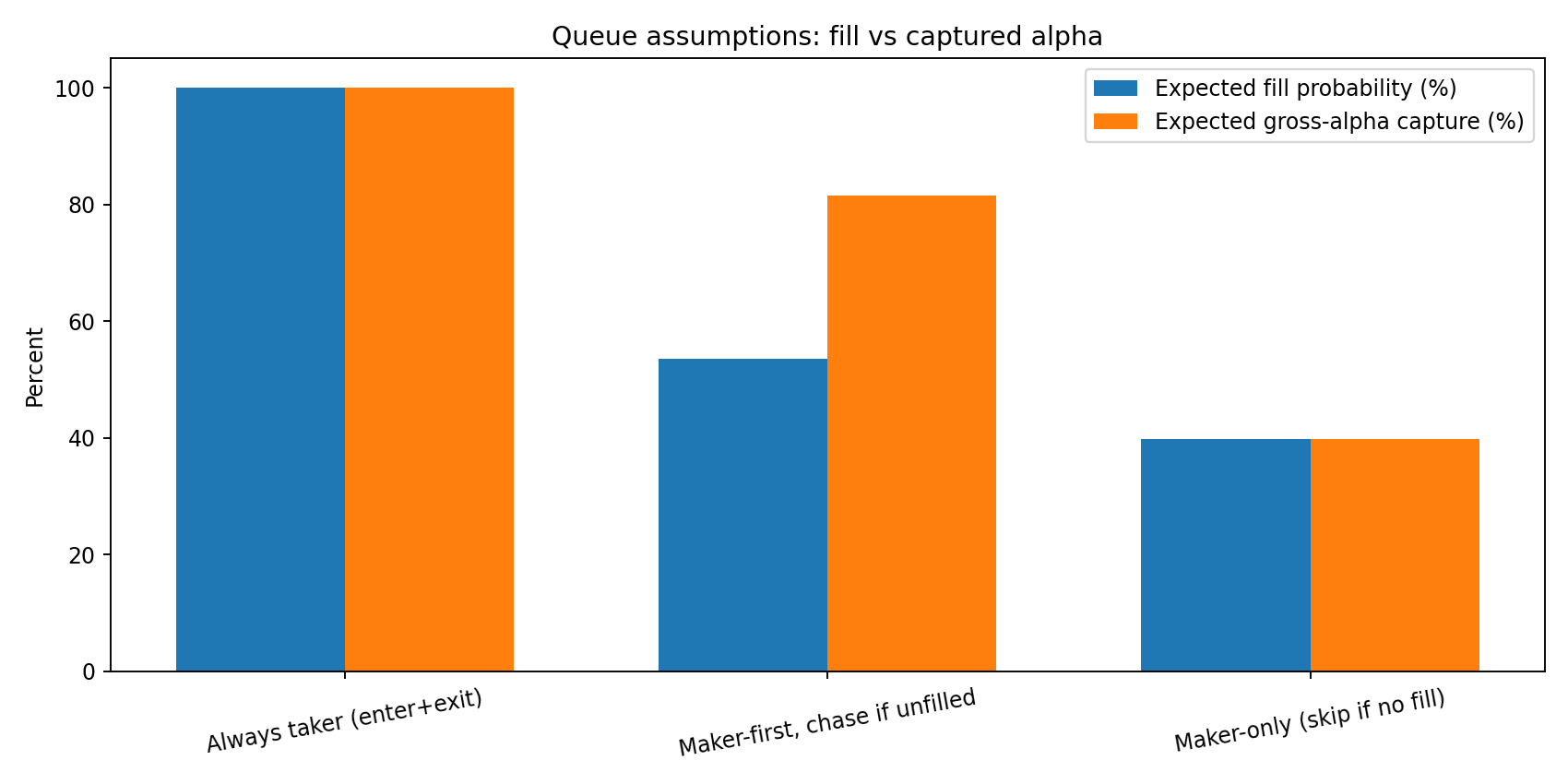

Fill/capture trade-off

Summary table

| Scenario | Avg bps/trade | Win rate | Final equity | Avg fill prob | Avg gross capture |

|---|---|---|---|---|---|

| Always taker | +0.24 | 49.6% | 0.979x | 100.0% | 100.0% |

| Maker-first, then chase | -5.75 | 47.9% | 0.920x | 53.6% | 81.4% |

| Maker-only passive | +3.45 | 50.4% | 1.036x | 39.8% | 39.8% |

Stationary-bootstrap 95% CI (mean bps/trade)

- Always taker: ([-28.36, +28.60]), (P(>0)=51.3%)

- Maker-first/chase: ([-30.52, +17.13]), (P(>0)=32.4%)

- Maker-only passive: ([-8.77, +15.16]), (P(>0)=72.7%)

Honest interpretation

- Maker-only “looks best” only because it trades much less.

- It captures ~40% of gross alpha and skips ~60% of opportunities.

- Lower cost helps, but opportunity loss is massive.

- Chasing missed maker fills is expensive.

- Once you add delayed-entry alpha decay + taker fallback costs, expectancy turns negative.

- Still not statistically decisive.

- Every CI still overlaps zero.

- This remains a research candidate, not a scale-up signal.

Reproducibility

In this folder:

analyze_maker_taker_queue.pyday18-maker-taker-queue-results.jsonday18-queue-equity-curves.pngday18-fill-capture-bars.png

Run:

python3 blog/posts/2026-03-03-maker-taker-queue/analyze_maker_taker_queue.pyNext step

The right next test is now obvious:

Replace range-based fill proxies with venue-specific microstructure assumptions (or full L2 replay where possible), then run the same walk-forward + bootstrap stack across venues.

Until then: no aggressive sizing.

References

- Politis, D.N. & Romano, J.P. (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

- Practical primer on stationary bootstrap: https://blogs.sas.com/content/iml/2021/01/20/stationary-bootstrap-sas.html

- Execution-cost modeling overview: https://www.quantstart.com/articles/Successful-Backtesting-of-Algorithmic-Trading-Strategies-Part-II/

Research only. Not financial advice.