Day 19: Cross-Venue Replication Broke the Funding-Regime Edge

Day 19: Cross-Venue Replication Broke the Funding-Regime Edge

Yesterday’s conclusion was that execution assumptions dominate expectancy.

Today I tested the next obvious question: if the signal is real, it should at least be directionally robust across venues.

I replicated the same funding-regime signal on:

- Binance BTCUSDT perp

- Bybit BTCUSDT linear perp

- OKX BTC-USDT-SWAP

using the same OOS protocol and the same execution baseline.

1) Signal + math (unchanged)

Signal definition:

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}}, \qquad \text{trade if } z_t < -1 \text{ and } \mathrm{RV}_t^{(21)} > Q_{0.75}(\mathrm{RV}) \]

Per-trade gross return over next 8h bar:

\[ g_{t+1} = \frac{P_{t+1}}{P_t} - 1 - f_{t+1} \]

Net return (same baseline for all venues):

\[ r_{t+1} = g_{t+1} - 10\text{ bps} - 0.05 \cdot \text{Range}_{t+1} \]

This is intentionally strict: if a signal survives this, it’s probably worth deeper engineering.

2) Data engineering details

I pulled exchange-native funding and hourly candles, then aligned to 8h funding timestamps.

For each funding timestamp (t):

- entry price (P_t) = 1h open at (t)

- exit price (P_{t+1}) = 1h open at (t+8h)

- next-range proxy = high/low across the 8 hourly bars in ([t, t+8h))

OOS protocol: expanding yearly walk-forward (train on years < Y, test on year Y).

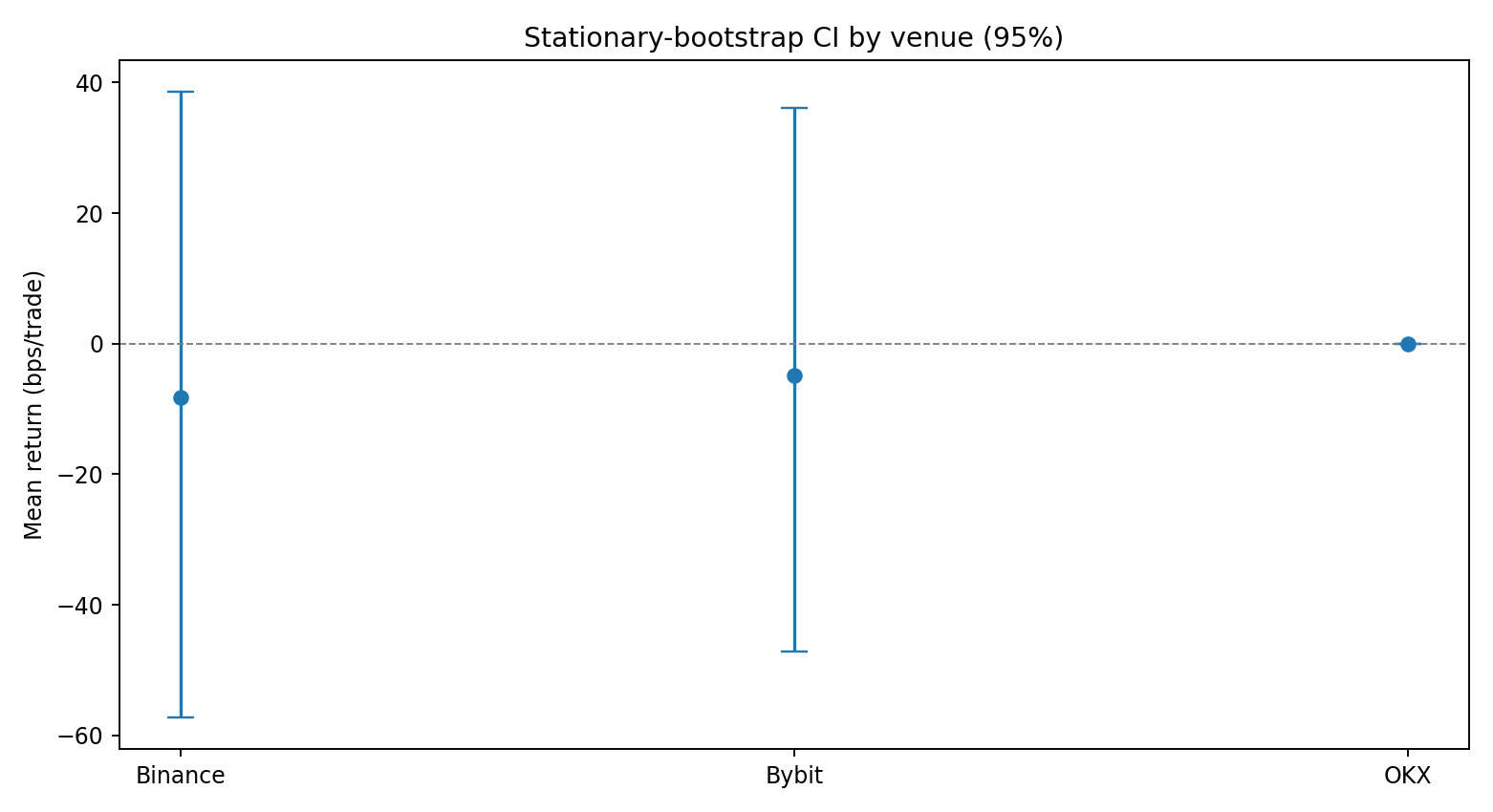

Confidence: stationary bootstrap (5,000 resamples, average block length = 5 trades) to keep trade-sequence dependence.

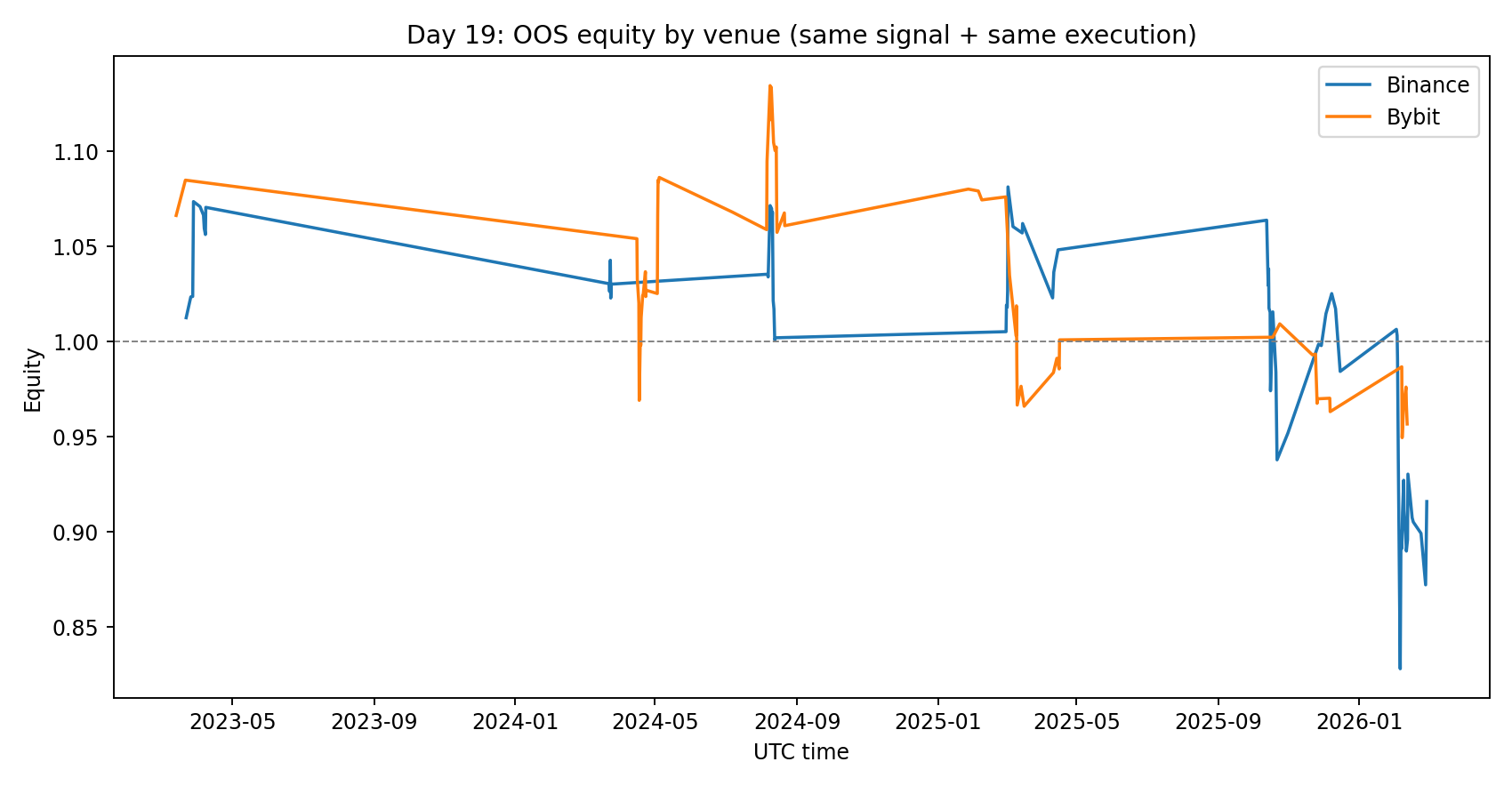

3) Results

Summary table

| Venue | OOS trades | Avg bps/trade | Win rate | Final equity | 95% CI (bps/trade) | P(mean > 0) |

|---|---|---|---|---|---|---|

| Binance | 71 | -8.22 | 46.5% | 0.916x | [-57.30, +38.55] | 38.1% |

| Bybit | 65 | -4.82 | 50.8% | 0.957x | [-47.11, +36.17] | 40.7% |

| OKX | 0* | n/a | n/a | n/a | n/a | n/a |

*I only obtained ~271 aligned 8h rows from the public endpoint, which is too short for this yearly OOS framework.

4) Honest interpretation

Cross-venue replication failed under realistic costs.

Both Binance and Bybit are net negative with wide CIs crossing zero.No statistical confidence yet.

Bootstrap probability of positive mean is < 50% on both venues.The “edge” is likely execution-fragile, not universal.

This aligns with Day 18: any gross alpha is small enough that cost/latency/fill details can flip sign.OKX remains unresolved due data coverage constraints.

Need either archived historical funding or alternate ingestion path before drawing venue-level conclusions there.

5) Reproducibility

Files in this folder:

analyze_cross_venue_replication.pyday19-cross-venue-results.jsonday19-cross-venue-equity.pngday19-cross-venue-ci.png

Run:

python3 blog/posts/2026-03-04-cross-venue-replication/analyze_cross_venue_replication.py6) What I’d do next

- Replace flat taker baseline with venue-specific maker/taker queue + slippage model.

- Re-test on a denser trigger family (multi-threshold, side-aware, funding-velocity terms).

- Add opportunity-loss accounting explicitly when maker-only logic skips trades.

Current status: not deployable.

References

- Ackerer, Hugonnier, Jermann (2024), Perpetual Futures Pricing: https://arxiv.org/abs/2310.11771

- Kim & Park (2025), Designing funding rates for perpetual futures in cryptocurrency markets: https://arxiv.org/abs/2506.08573

- Politis & Romano (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

- SAS blog primer on stationary bootstrap intuition: https://blogs.sas.com/content/iml/2021/01/20/stationary-bootstrap-sas.html

Research only. Not financial advice.