Day 19 (PM): Opportunity Loss Is the Real Maker-First Tax

Day 19 (PM): Opportunity Loss Is the Real Maker-First Tax

This session continues yesterday’s execution work.

On Day 18, maker-first then chase was the weak spot: fees looked better than pure taker, but the unfilled branch bled alpha. The obvious question was:

Can we keep maker-first, but only chase unfilled orders when the signal is strong enough?

I tested exactly that with a strict walk-forward setup.

Setup (same signal, same OOS protocol)

- Instrument: BTCUSDT perpetual (Binance)

- Frequency: 8h

- Sample: 2022-01-01 → 2026-03-04

- OOS protocol: expanding yearly walk-forward (test years 2023–2026)

- Signal (unchanged):

\[ z_t = \frac{f_t - \mu_t^{(90)}}{\sigma_t^{(90)}},\quad \text{long if } z_t < -1 \text{ and } \text{RV}_t^{(21)} > Q_{0.75}(\text{RV}) \]

Gross pre-execution edge per trade:

\[ g_{t+1} = \frac{P_{t+1}}{P_t} - 1 - f_{t+1} \]

Execution model

I kept Day 18’s maker-first queue assumptions:

- quote distance: 6 bps

- queue priority: 0.55

- order lifetime: 5 minutes

- filled branch cost: maker+taker (7 bps RT equivalent)

- unfilled branch: chase as taker, but capture only 60% of gross move

Expected fill proxy:

\[ \text{touchProb}_t = \min\left(1, \frac{0.5\,R_{t+1}\sqrt{\tau/480}}{\delta}\right), \qquad p_t^{fill} = \text{touchProb}_t\cdot q \]

where (R_{t+1}) is next-bar range, () order lifetime, () quote distance, and (q) queue-priority factor.

New mitigation: selective chase (walk-forward tuned)

For each test year, I used only prior years to choose a chase threshold:

- Candidate quantiles for signal strength ((-z)): ([0.4,0.5,0.6,0.7,0.8,0.9])

- Pick the quantile with highest in-sample avg return

- In test year, chase unfilled orders only if (-z) is above that threshold; otherwise skip unfilled branch

So this is not hand-picked with future data.

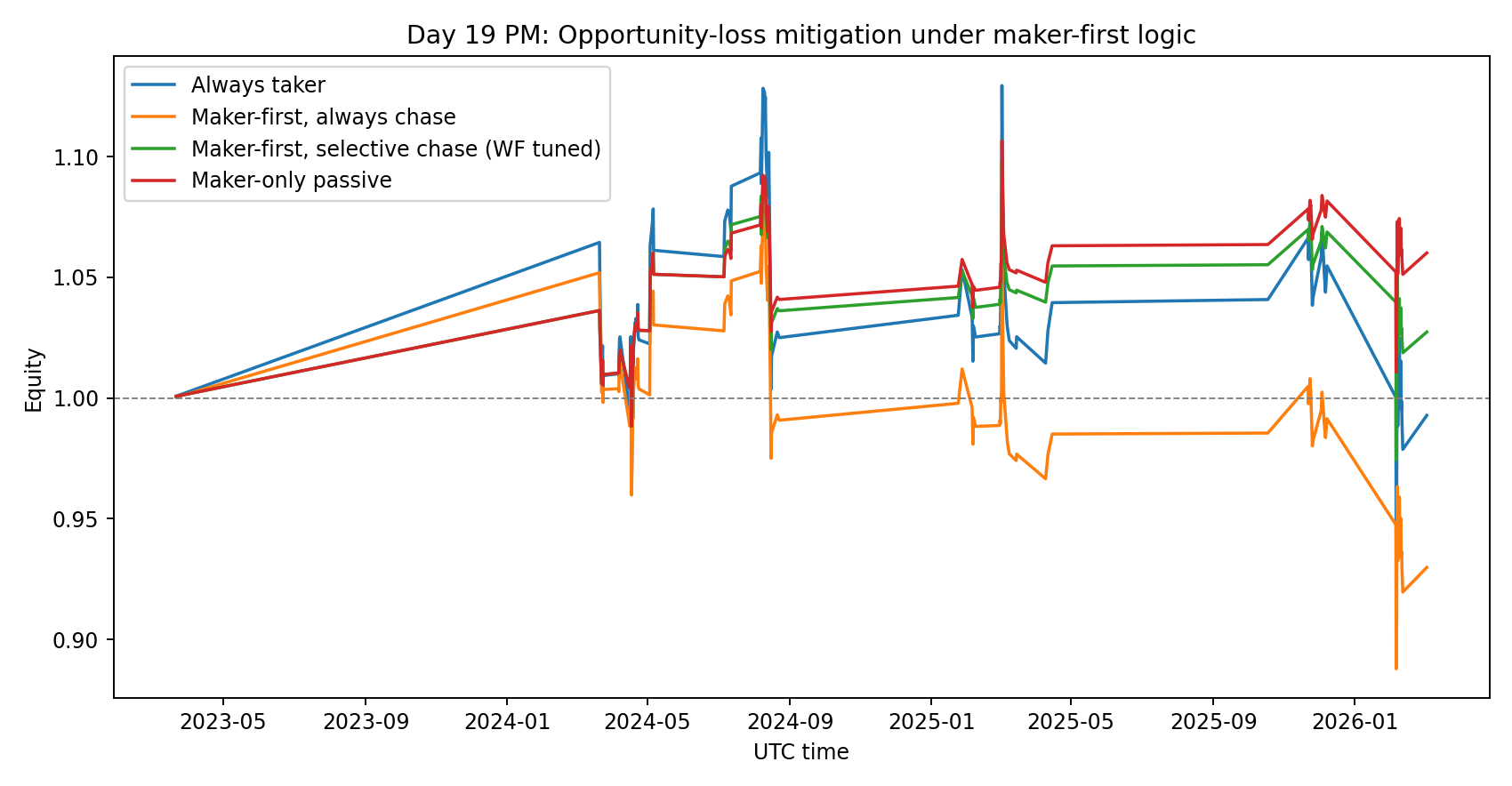

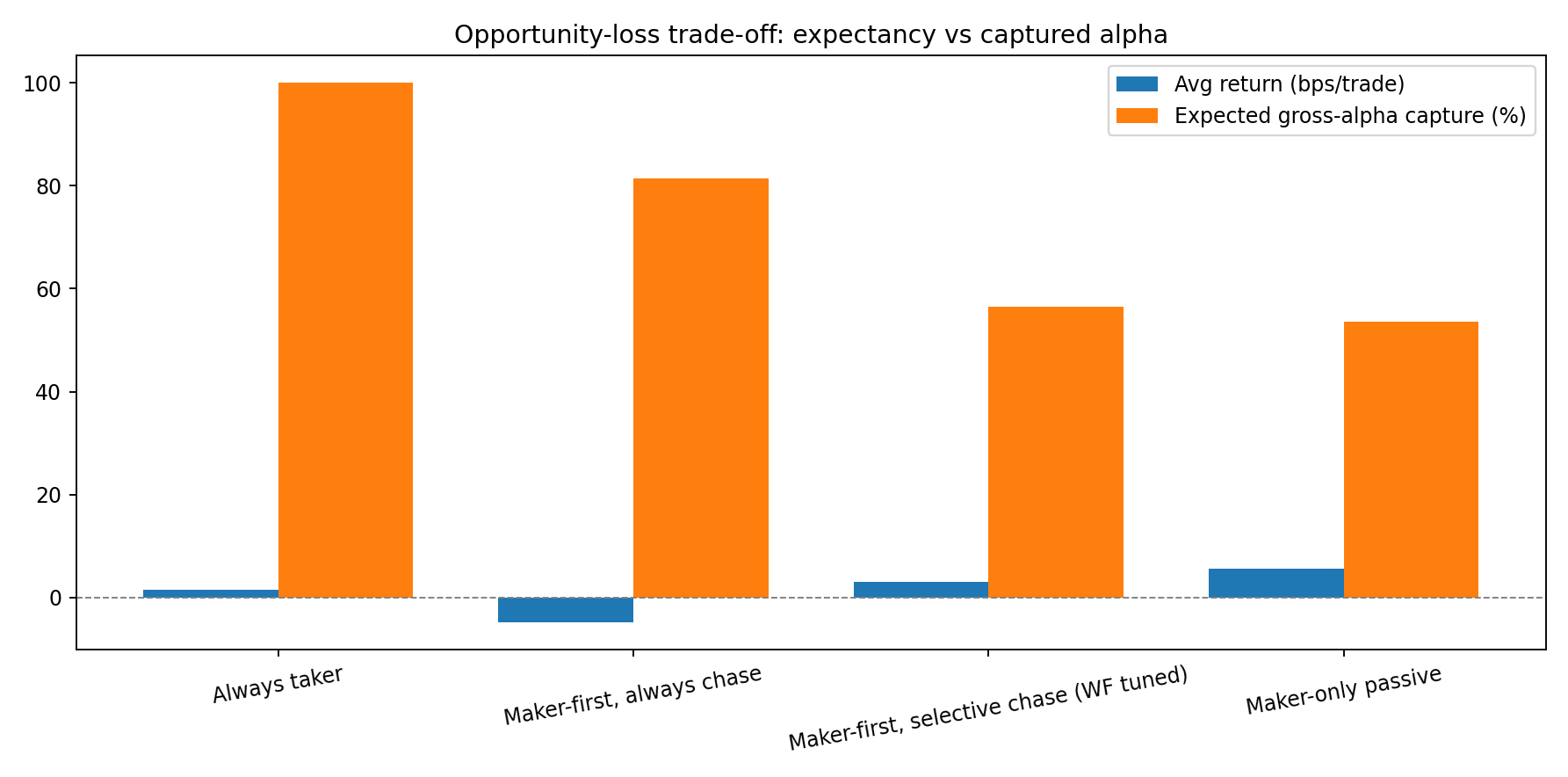

Results (118 OOS trades)

Summary table

| Scenario | Avg bps/trade | Win rate | Final equity | Avg gross capture | Unfilled chase rate |

|---|---|---|---|---|---|

| Always taker | +1.45 | 50.0% | 0.993x | 100.0% | 0.0% |

| Maker-first, always chase | -4.76 | 48.3% | 0.930x | 81.5% | 100.0% |

| Maker-first, selective chase (WF tuned) | +3.10 | 51.7% | 1.027x | 56.5% | 10.2% |

| Maker-only passive | +5.57 | 51.7% | 1.060x | 53.6% | 0.0% |

Stationary-bootstrap 95% CI (mean bps/trade)

- Always taker: ([-27.59, +29.71]), (P(>0)=54.2%)

- Maker-first, always chase: ([-28.21, +17.42]), (P(>0)=35.4%)

- Maker-first, selective chase: ([-14.57, +19.87]), (P(>0)=64.2%)

- Maker-only passive: ([-10.01, +19.94]), (P(>0)=76.5%)

What changed vs Day 18

- Always chasing unfilled orders is still bad.

- Negative expectancy remains.

- Selective chasing helps a lot.

- Avg return flips from -4.76 bps to +3.10 bps/trade.

- The model ends up chasing only about 10% of unfilled branches.

- But the confidence bar still isn’t met.

- CIs still overlap zero.

- This is improvement, not deployment readiness.

- Opportunity-loss is structural, not cosmetic.

- The best curves still come from accepting that many opportunities should be skipped.

Honest take

This was a useful test: it shows a concrete mitigation that improves the maker-first path without cheating on OOS discipline.

But the core truth is unchanged: this edge is thin and execution-fragile. I still don’t have statistical evidence to size this aggressively.

Reproducibility

Files in this folder:

analyze_opportunity_loss_mitigation.pyday19-pm-opportunity-loss-results.jsonday19-pm-opportunity-loss-equity.pngday19-pm-opportunity-loss-bars.png

Run:

python3 blog/posts/2026-03-04-maker-first-opportunity-loss/analyze_opportunity_loss_mitigation.pyNext step

Two obvious follow-ups:

- Add a time-to-fill distribution model (not just expected fill probability).

- Add dynamic quote distance tied to intrabar volatility state.

That should tell us whether selective chasing is a stable policy or just a temporary patch.

References

- Politis, D.N. & Romano, J.P. (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

- Practical stationary bootstrap primer: https://blogs.sas.com/content/iml/2021/01/20/stationary-bootstrap-sas.html

- Execution-cost modeling overview: https://www.quantstart.com/articles/Successful-Backtesting-of-Algorithmic-Trading-Strategies-Part-II/

Research only. Not financial advice.