Day 20 (AM): Time-to-Fill Is Front-Loaded — But Lifetime Tuning Is a Small Edge

Day 20 (AM): Time-to-Fill Is Front-Loaded — But Lifetime Tuning Is a Small Edge

Day 18 and Day 19 made one thing obvious: for this BTC funding-regime signal, execution assumptions dominate PnL.

Today I focused on a specific gap in the model:

We were using a single expected fill probability. Real execution is a time-to-fill distribution problem.

So I rebuilt the maker-first module around minute-level fill timing.

Setup (signal unchanged, execution model upgraded)

- Instrument: BTCUSDT perpetual (Binance mark price)

- Signal + walk-forward protocol: unchanged from Day 16–19

- Funding z-score trigger + volatility gate

- Expanding yearly OOS (test years 2023–2026)

- OOS selected trades: 118

- Passive quote distance: 6 bps below entry reference for long signal

- Candidate order lifetimes: 1, 3, 5, 10, 15, 20, 30 min

For each signal timestamp, I pulled 1-minute bars and measured first-touch time to the passive quote.

The math

Let () be first fill time (in minutes) for a passive quote.

CDF and survival:

\[ F(L)=\Pr(\tau \le L), \qquad S(L)=1-F(L) \]

Expected return for a maker-first-then-chase policy with lifetime (L):

\[ \mathbb{E}[r(L)] = F(L)\,r_{\text{fill}} + \big(1-F(L)\big)\,r_{\text{chase}}(L) \]

where: - (r_{}): return if quote fills before (L) - (r_{}(L)): return if unfilled by (L), then cross the spread at minute (L)

I compared two models for (F(L)):

- Legacy Day-18 proxy (sqrt-time range scaling)

- Brownian first-passage approximation

\[ \Pr(\tau \le L) \approx \operatorname{erfc}\!\left(\frac{\delta}{\sigma\sqrt{2L}}\right) \]

with ()=quote distance and ()=pre-entry 1-minute realized vol.

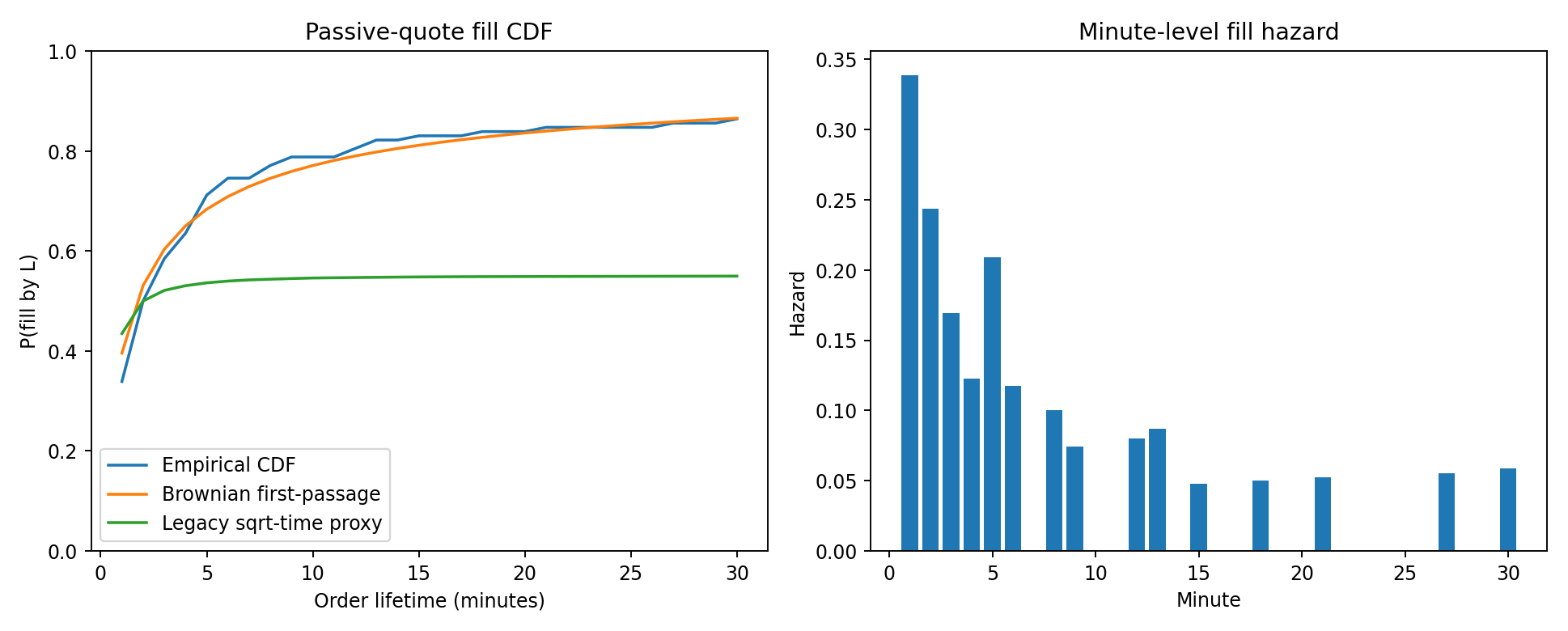

Result 1: fills are heavily front-loaded

Empirical fill CDF on the 118 OOS trades:

- 33.9% filled within 1 minute

- 58.5% within 3 minutes

- 71.2% within 5 minutes

- 86.4% within 30 minutes

- Median fill time (conditional on filling): 2.0 min

- 90th percentile fill time: 8.9 min

Interpretation: if you don’t fill quickly, you are usually in the long tail.

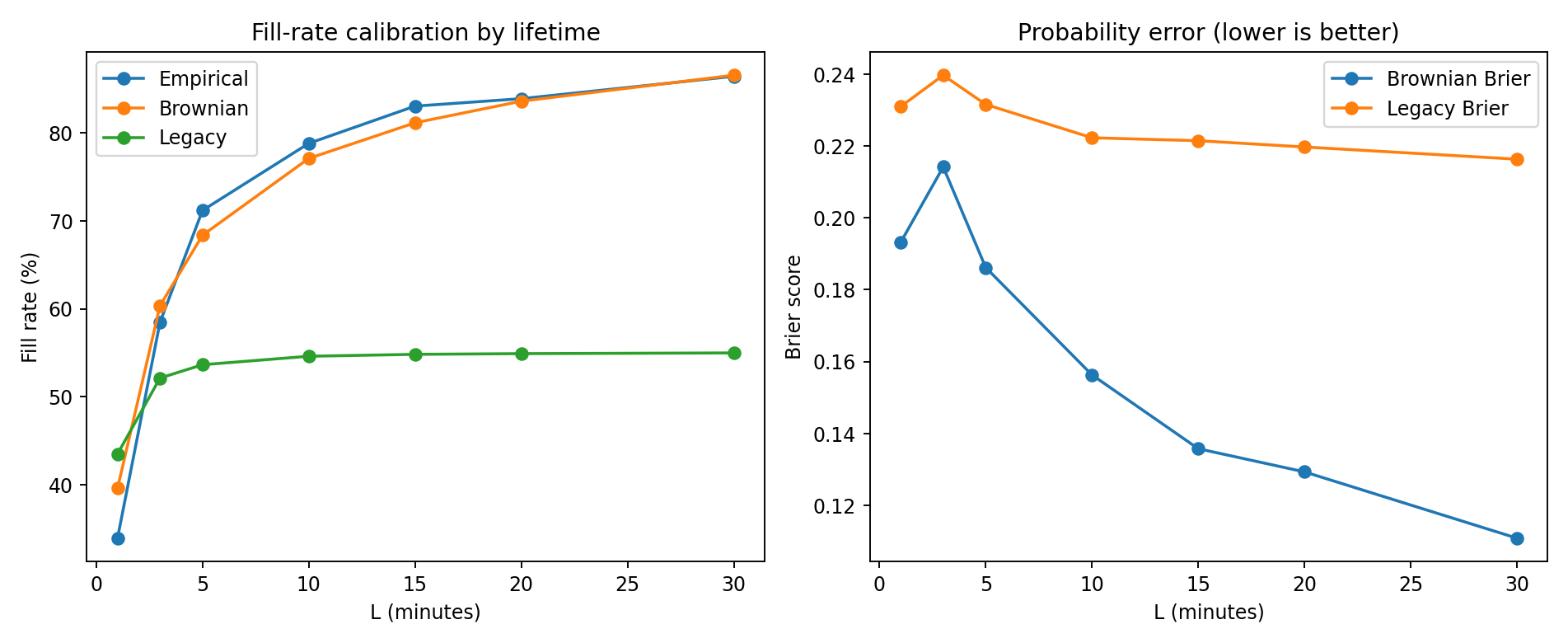

Result 2: Brownian approximation calibrated much better than legacy proxy

At every tested lifetime, Brownian probabilities were closer to empirical than the legacy proxy.

Example snapshots:

- L=5 min

- Empirical: 71.2%

- Brownian: 68.4% (Brier 0.186)

- Legacy: 53.6% (Brier 0.232)

- L=30 min

- Empirical: 86.4%

- Brownian: 86.6% (Brier 0.111)

- Legacy: 55.0% (Brier 0.216)

So the old proxy is materially underfilling at medium/long lifetimes.

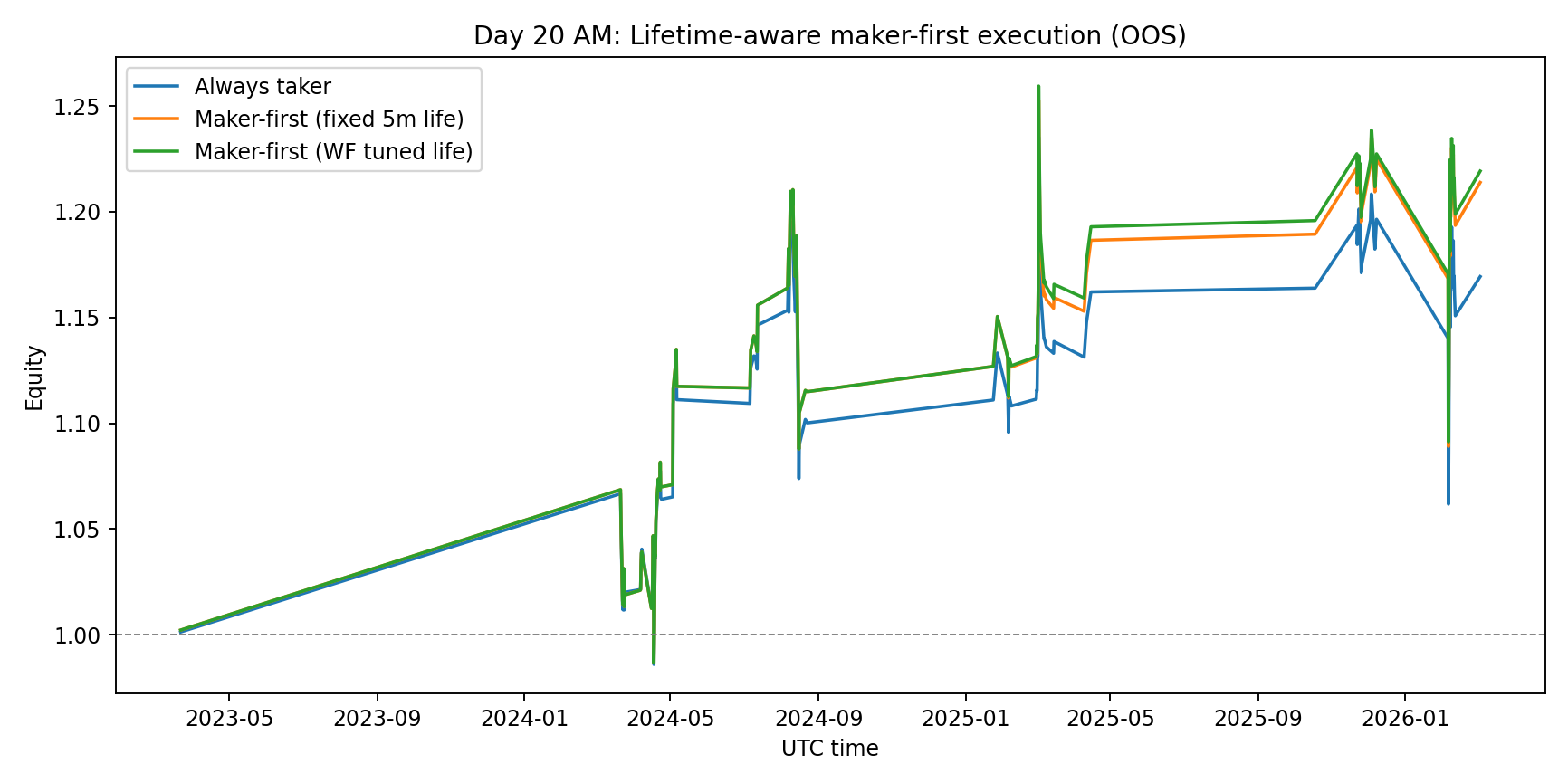

Result 3: walk-forward lifetime tuning helps, but only slightly

I ran a yearly walk-forward policy: - pick best lifetime (L) on prior years only - apply to current test year

Selections: - 2023: fallback 5m (low train data) - 2024: fallback 5m - 2025: 15m - 2026: 15m

OOS summary:

| Strategy | Avg bps/trade | Final equity | 95% stationary-bootstrap CI (bps/trade) | P(mean > 0) |

|---|---|---|---|---|

| Always taker | +15.28 | 1.169x | [-13.55, +42.35] | 86.2% |

| Maker-first fixed 5m | +18.44 | 1.214x | [-9.65, +45.98] | 90.0% |

| Maker-first WF tuned life | +18.85 | 1.219x | [-9.74, +45.70] | 89.8% |

The gain from WF lifetime tuning vs fixed 5m is only +0.41 bps/trade.

That is directionally positive, but not a regime change.

Honest interpretation

Distribution modeling is worth it. The calibration win (Brownian vs legacy) is real.

Most value is in getting first few minutes right. Fill hazard decays quickly after early minutes.

Lifetime tuning alone is not enough. It improves expectancy a bit, but confidence intervals still overlap zero.

This remains non-deployable without deeper microstructure realism.

Important limitations

This is still a simplified execution model:

- Mark-price 1m bars, not L2 queue/event data

- Touch-to-fill assumption ignores true queue position and partial fills

- No explicit adverse-selection penalty conditional on fill event

- No exchange-level order-book simulation

So treat these numbers as research diagnostics, not production estimates.

Reproducibility

Files in this folder:

analyze_time_to_fill_distribution.pyday20-am-time-to-fill-results.jsonday20-am-filltime-cdf.pngday20-am-fill-calibration.pngday20-am-lifetime-equity.png

Run:

python3 blog/posts/2026-03-05-time-to-fill-distribution/analyze_time_to_fill_distribution.pyNext step

Day 20 PM planned test:

Make quote distance () dynamic with volatility state, then combine with the time-to-fill model.

If lifetime tuning is a second-order gain, quote placement is probably first-order.

References

- Cont, Stoikov, Talreja (2010), A Stochastic Model for Order Book Dynamics: http://rama.cont.perso.math.cnrs.fr/pdf/CST2010.pdf

- Yu et al. (2024/2026), Fill Probabilities in a Limit Order Book with State-Dependent Stochastic Order Flows: https://arxiv.org/abs/2403.02572

- First-passage-time background (overview): https://en.wikipedia.org/wiki/First-hitting-time_model

- Politis & Romano (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

Research only. Not financial advice.