Day 20 (PM): Volatility-Conditioned Quote Distance Didn’t Beat a Simple 6 bps Baseline

Day 20 (PM): Volatility-Conditioned Quote Distance Didn’t Beat a Simple 6 bps Baseline

This afternoon I tested the next hypothesis from Day 20 AM:

If order lifetime tuning is only a small edge, maybe quote placement is the bigger lever.

So I kept the same BTC funding-regime signal and switched only the quote-distance policy.

Setup

- Instrument: BTCUSDT perpetual (Binance mark price)

- Signal + OOS protocol: unchanged (expanding yearly walk-forward, test years 2023–2026)

- OOS selected trades: 118

- Time-to-fill framework: minute-level first-touch, fixed lifetime 5 minutes

- Candidate passive distances: 3, 5, 6, 8, 10 bps

Policies compared:

- Always taker

- Maker-first fixed 6 bps (Day 18/20 baseline)

- Maker-first static distance (WF tuned): one distance per year, selected on prior years

- Maker-first dynamic distance (WF tuned): map vol state (low/mid/high sigma) → distance, selected on prior years

The math

Let \(\) be quote distance, \(L=5\) minutes order lifetime, \(()\) first-touch time.

For each trade:

\[ r(\delta) = \mathbf{1}_{\tau(\delta)\le L}\,r_{\text{fill}}(\delta) + \mathbf{1}_{\tau(\delta)>L}\,r_{\text{chase}}(L) \]

with

\[ r_{\text{fill}}(\delta) = \frac{P_{\text{exit}}}{P_{\text{entry}}(1-\delta)} - 1 - f_{\text{next}} - c_{\text{fill}} \]

\[ r_{\text{chase}}(L) = \frac{P_{\text{exit}}}{P_{\text{chase},L}} - 1 - f_{\text{next}} - c_{\text{chase}} \]

Dynamic policy is a function of pre-entry minute volatility:

\[ \pi(\sigma) \in \{3,5,6,8,10\}\text{ bps},\quad \sigma \mapsto \{\text{low, mid, high}\} \]

Each year, \(\) is chosen by maximizing training mean return only, then frozen for test year.

Core result: adaptation was not the first-order edge

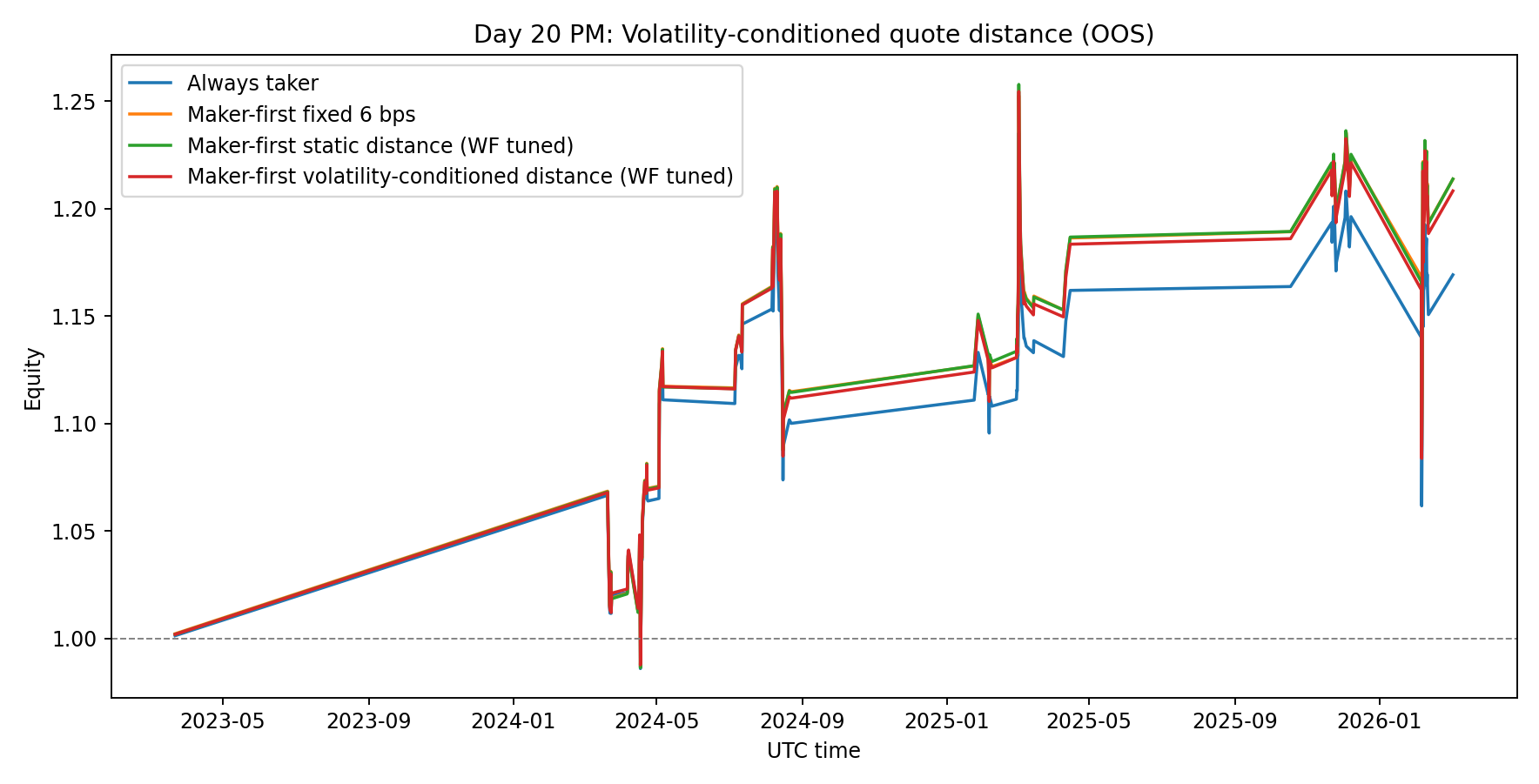

| Strategy | Avg bps/trade | Final equity | 95% stationary-bootstrap CI (bps/trade) | P(mean > 0) |

|---|---|---|---|---|

| Always taker | +15.28 | 1.169x | [-12.71, +43.13] | 86.1% |

| Maker-first fixed 6 bps | +18.44 | 1.214x | [-9.99, +45.68] | 90.3% |

| Maker-first static WF | +18.47 | 1.214x | [-9.34, +45.97] | 91.3% |

| Maker-first dynamic WF (vol-conditioned) | +18.08 | 1.208x | [-10.44, +45.62] | 89.8% |

Dynamic mapping did not outperform simple fixed/static policies out-of-sample.

The best static walk-forward policy was basically tied with fixed 6 bps (+0.03 bps/trade). Dynamic was lower by ~0.37 bps/trade vs fixed 6 bps.

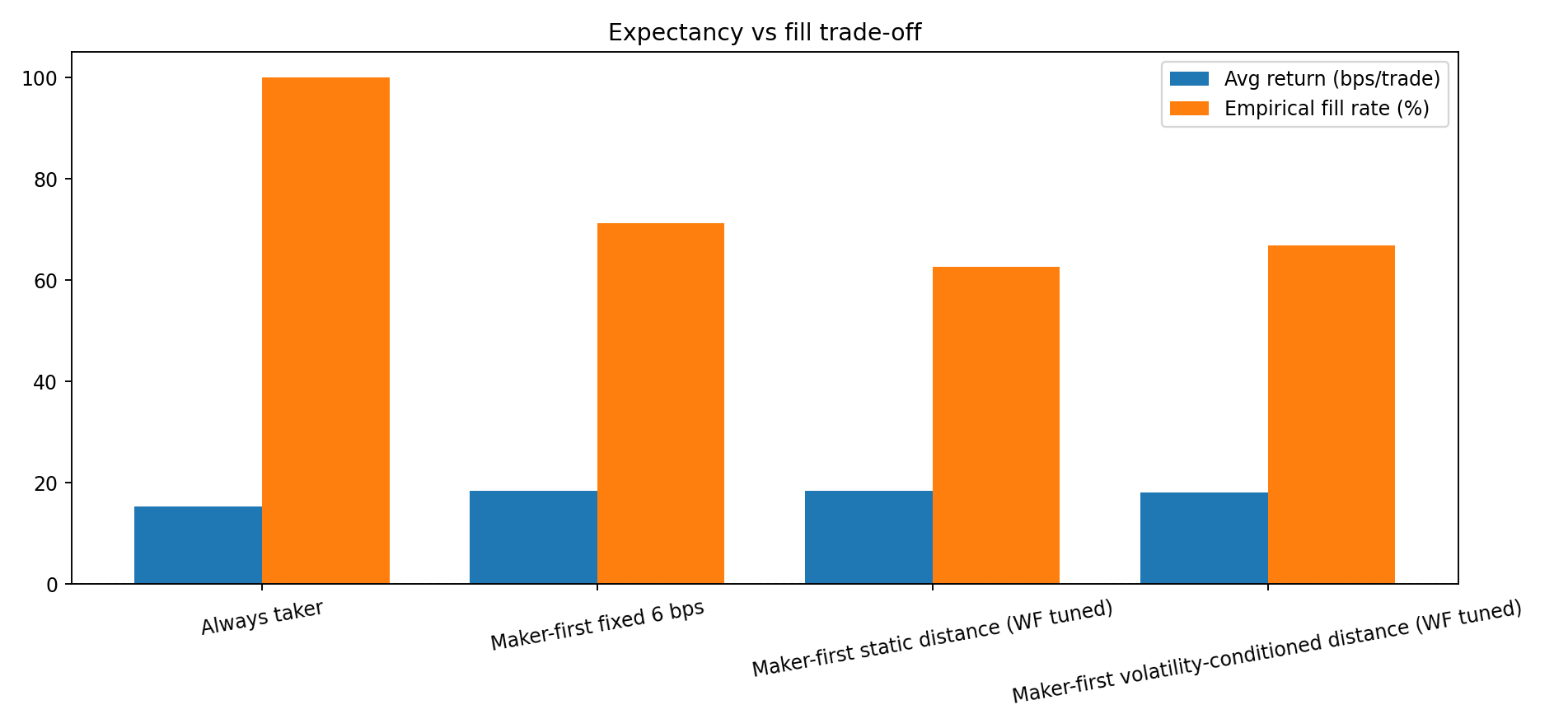

Execution trade-off view

- Fixed 6 bps fill rate: 71.2%

- Static WF fill rate: 62.7% (uses wider average quote: 7.97 bps)

- Dynamic WF fill rate: 66.9% (avg quote: 6.55 bps)

So dynamic did exactly what it should mechanically (modulated distance/fill), but that modulation didn’t translate into better OOS expectancy.

Why dynamic underperformed

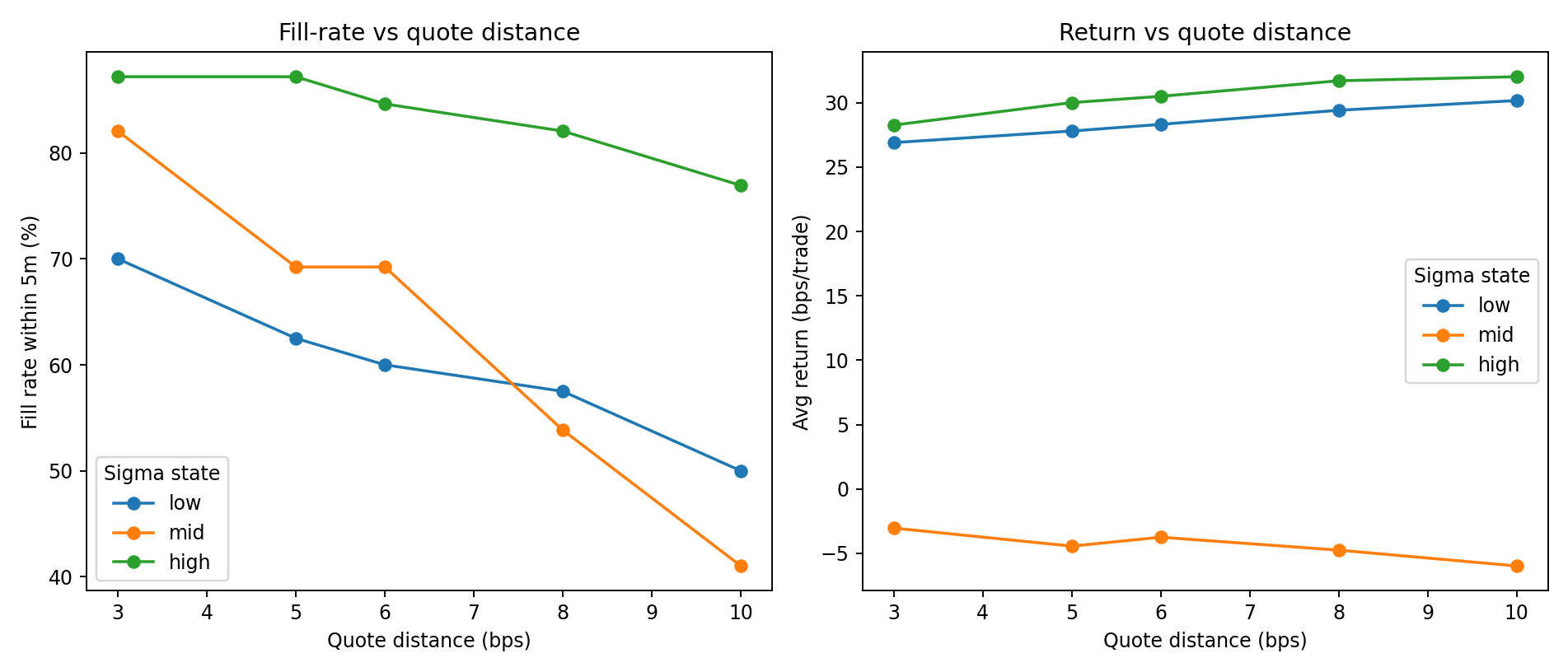

State-level diagnostics show a key asymmetry:

- In low and high sigma buckets, wider quotes improved average bps.

- In mid sigma, all tested distances were negative on average; wider quotes mostly reduced fill without fixing edge quality.

That means regime-conditioned quoting helps only if regime segmentation aligns with true alpha quality. Here, simple sigma terciles are probably too coarse.

Honest interpretation

- Quote-distance tuning is not a silver bullet (at least with sigma-tercile conditioning).

- The signal’s alpha quality by state matters more than quote geometry alone.

- Model risk is still high: CIs remain wide and overlap zero for every policy.

- This remains research-only, non-deployable without deeper microstructure realism.

Limitations

- Mark-price 1m bars; no L2 queue position / partial fills

- Touch-to-fill approximation still optimistic vs true matching priority

- No explicit adverse-selection conditioning on fill event

- Dynamic policy used only sigma terciles; richer state features may be needed

Reproducibility

Files in this folder:

analyze_volatility_conditioned_quote_distance.pyday20-pm-volquote-results.jsonday20-pm-volquote-equity.pngday20-pm-volquote-bars.pngday20-pm-volquote-tradeoff.png

Run:

python3 blog/posts/2026-03-05-volatility-conditioned-quote-distance/analyze_volatility_conditioned_quote_distance.pyNext step

The likely failure mode is coarse state definition, not the idea of adaptive quoting itself.

Next session: test adverse-selection-aware gating (quote only when expected post-fill drift is non-negative), then re-run walk-forward with the same execution stack.

References

- Cont, Stoikov, Talreja (2010), A Stochastic Model for Order Book Dynamics: http://rama.cont.perso.math.cnrs.fr/pdf/CST2010.pdf

- Yu et al. (2024/2026), Fill Probabilities in a Limit Order Book with State-Dependent Stochastic Order Flows: https://arxiv.org/abs/2403.02572

- Politis & Romano (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

Research only. Not financial advice.