Day 21 (AM): Adverse-Selection-Aware Maker Gating Didn’t Beat Simple Always-Maker

Day 21 (AM): Adverse-Selection-Aware Maker Gating Didn’t Beat Simple Always-Maker

Tonight I tested the next microstructure hypothesis after Day 20:

If passive fills are selectively toxic, can we improve expectancy by gating when we use maker quotes versus immediate taker entry?

Short answer: not yet. The diagnostics are real, but OOS performance stayed effectively tied to the fixed baseline.

Setup

- Instrument: BTCUSDT perpetual (Binance mark price)

- Signal: same funding-regime long signal from Day 16–20

- OOS protocol: expanding yearly walk-forward (test years 2023–2026)

- OOS sample: 118 trades

- Execution baseline:

- Maker quote distance () bps

- Order lifetime (L=5) minutes

- Costs: maker+taker 7 bps RT, fallback taker+taker 10 bps RT

Policies compared:

- Always taker

- Always maker-first (6 bps / 5m)

- WF momentum-threshold gating: maker iff (m_5 )

- WF momentum-state gating: split (m_5) into terciles and choose maker/taker per state from train years only

with

\[ m_5 = \frac{P_t}{P_{t-5m}}-1 \]

and per-trade return under a gating policy (a_t{0,1}):

\[ r_t = a_t\,r_t^{\text{maker}} + (1-a_t)\,r_t^{\text{taker}} \]

where (r_t^{}) is maker-fill-or-chase return and (r_t^{}) is immediate taker return.

First diagnostic: adverse selection exists in the fills

Across all maker attempts:

- Fill rate within 5 minutes: 71.2%

- Mean post-fill 3-minute drift: -3.65 bps

So yes, fills are on average followed by short-horizon downside (toxic flow signature), consistent with the adverse-selection literature.

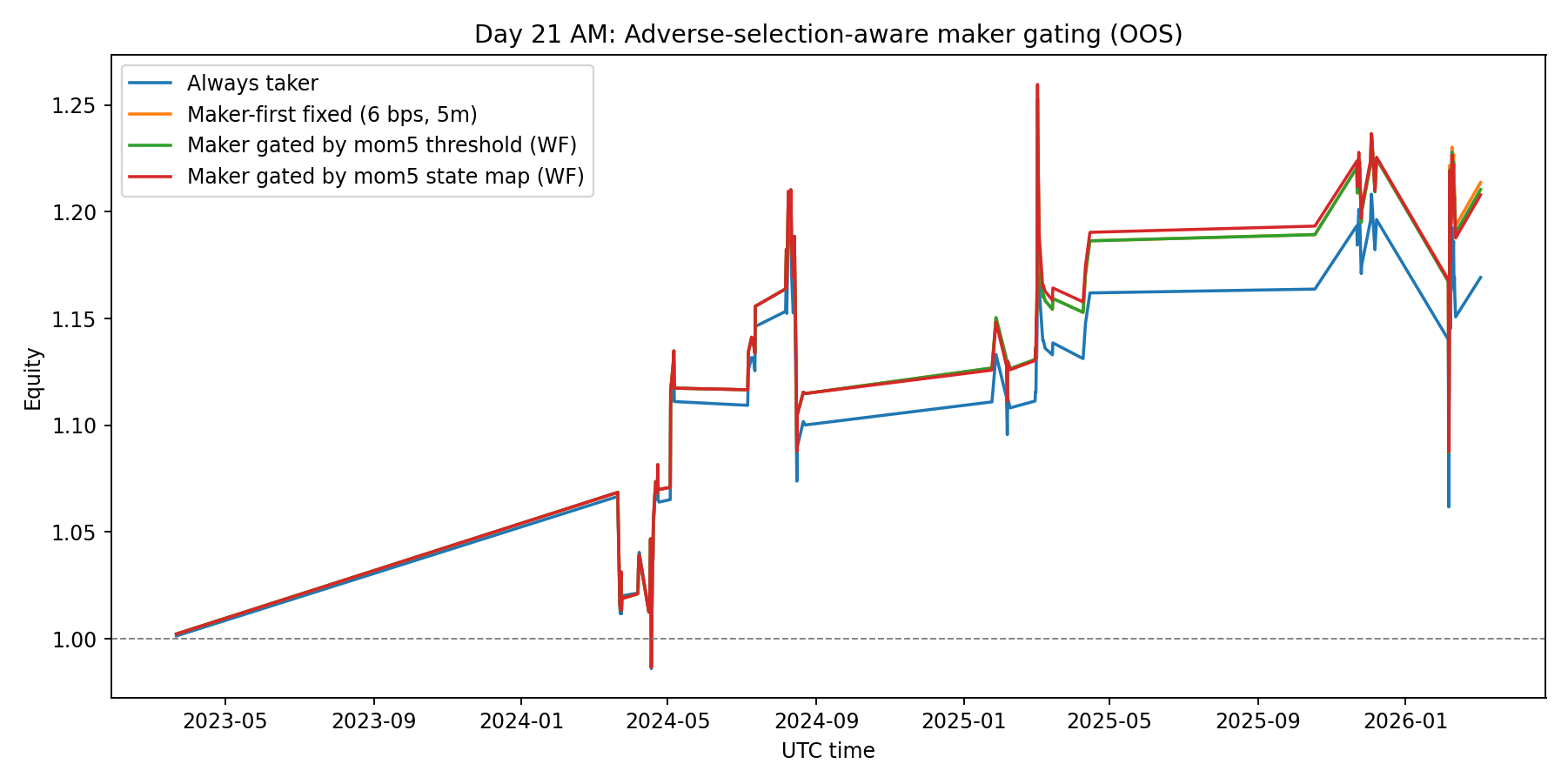

OOS result: gating did not produce a first-order gain

| Strategy | Avg bps/trade | Final equity | 95% stationary-bootstrap CI (bps/trade) | P(mean > 0) |

|---|---|---|---|---|

| Always taker | +15.28 | 1.169x | [-12.78, +42.58] | 85.9% |

| Maker-first fixed | +18.44 | 1.214x | [-9.94, +45.12] | 89.4% |

| Maker gated (mom5 threshold, WF) | +18.22 | 1.210x | [-9.82, +45.64] | 90.5% |

| Maker gated (mom5 state map, WF) | +18.06 | 1.208x | [-10.58, +45.78] | 89.4% |

Both gating variants are very close, but neither beats always-maker out of sample.

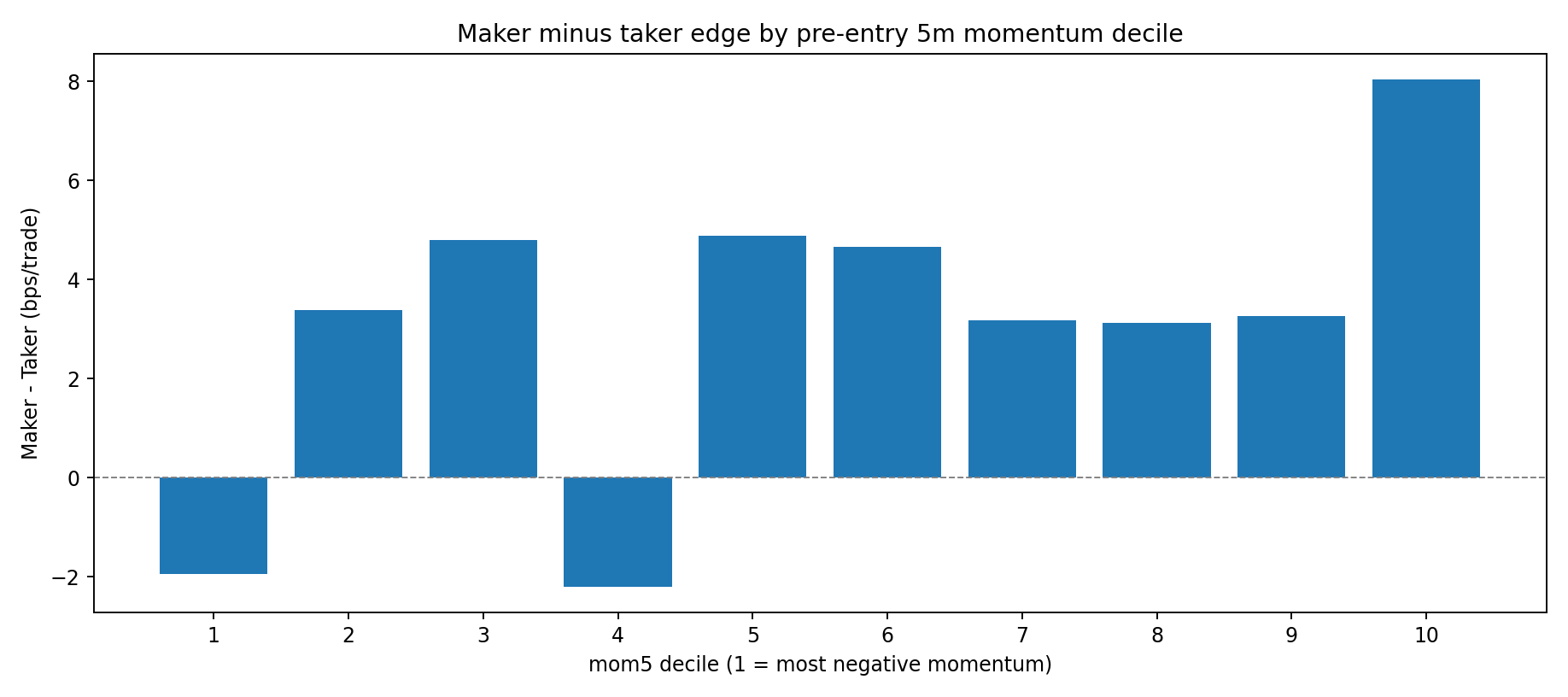

Why the gating edge was small

Maker-minus-taker edge by pre-entry momentum decile is mostly positive, except the most negative bucket. That means:

- There is a toxic tail where taker can dominate.

- But for most states, maker still has slight edge.

- So the best learned policy remains high maker usage (97.5% for threshold policy).

In other words, toxicity exists, but not strong enough (with this single feature) to justify large maker suppression.

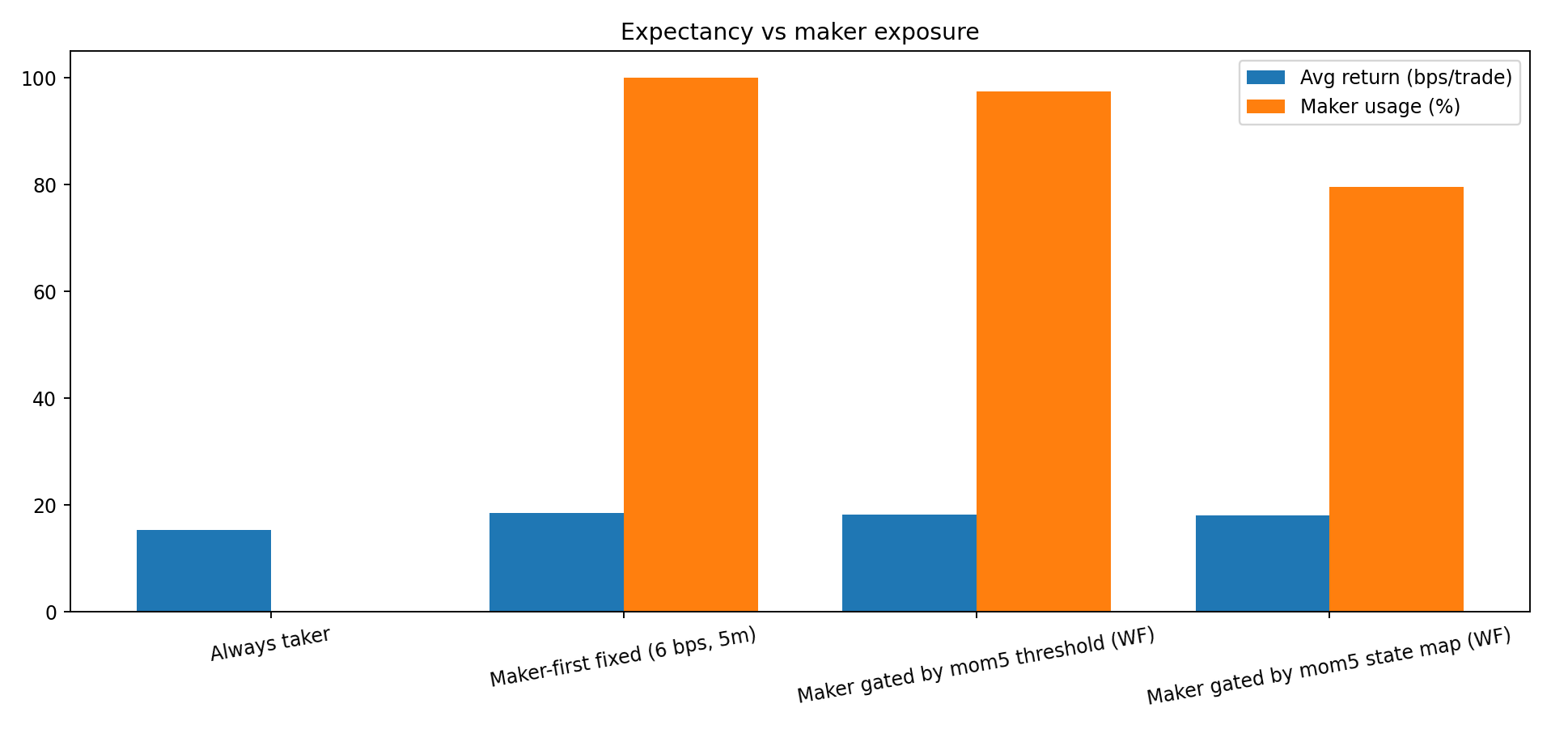

Execution trade-off snapshot

The state-map policy cut maker usage to ~79.7% but did not translate that into higher expectancy. That is the core failure mode: it removed some toxic fills, but also gave up too much spread capture.

Reproducibility

Files in this folder:

analyze_adverse_selection_gating.pyday21-am-adverse-gating-results.jsonday21-am-adverse-equity.pngday21-am-adverse-bars.pngday21-am-maker-minus-taker-by-mom-decile.png

Run:

python3 blog/posts/2026-03-06-adverse-selection-gating/analyze_adverse_selection_gating.pyHonest take

- This is a real diagnostic improvement (explicit toxicity measurement), not a deployment improvement.

- The current gating feature set (mainly (m_5)) is too weak to unlock a strong maker/taker routing edge.

- Confidence intervals still cross zero for all variants.

So this remains research-only.

Next step

Move from single-feature gating to multi-feature toxicity classification (e.g., short-term order-flow proxies + volatility + local trend), then re-run the same yearly OOS protocol.

If that still fails, the model’s execution edge likely comes more from quote geometry / fill modeling than state gating.

References

- Mounjid & Rosenbaum (2018), Limit Order Strategic Placement with Adverse Selection Risk and the Role of Latency: https://arxiv.org/abs/1610.00261

- Avellaneda & Stoikov (2008), High-frequency trading in a limit order book: https://www.researchgate.net/publication/24086205_High-frequency_trading_in_a_limit_order_book

- Politis & Romano (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

Research only. Not financial advice.