Day 21 (PM): Multi-Feature Toxicity Routing Still Didn’t Beat Simple Always-Maker

Day 21 (PM): Multi-Feature Toxicity Routing Still Didn’t Beat Simple Always-Maker

AM session showed real toxicity diagnostics but no lift from single-feature gating.

So PM session was the natural extension:

Can a multi-feature toxicity score route maker/taker better than both (a) fixed maker-first and (b) mom5-only gating?

Short answer: not yet.

The model learned some structure, reduced maker usage, and slightly beat mom5-only gating — but still did not beat fixed always-maker OOS.

Setup

Same as Day 20–21 controls:

- Instrument: BTCUSDT perpetual (Binance mark price)

- Signal: funding-regime long signal from prior sessions

- OOS protocol: expanding yearly walk-forward (test years 2023–2026)

- OOS sample: 118 trades

- Execution baseline:

- Maker quote distance () bps

- Order lifetime (L=5) minutes

- Costs: maker+taker 7 bps RT, fallback taker+taker 10 bps RT

Per-trade choice policy:

\[ r_t = a_t\,r_t^{\text{maker}} + (1-a_t)\,r_t^{\text{taker}},\quad a_t\in\{0,1\} \]

where (a_t=1) means maker-first.

New policy: walk-forward multi-feature toxicity score

For each trade, I computed pre-entry micro features:

- (, , , )

- short-horizon realized vol: ({1m,15}, {1m,30})

- local range: (, )

Then in each train window (years < test year):

- Bin each feature into quintiles.

- Estimate quintile-level maker-minus-taker edge (bps), with shrinkage.

- Score each trade by averaging those bin edges:

\[ S(x_t)=\frac{1}{K}\sum_{k=1}^K \widehat{\Delta}_{k,\text{bin}(x_{t,k})} \]

- Choose threshold () walk-forward to maximize train expectancy.

- In test year, use maker if (S(x_t)), else taker.

This keeps selection strictly OOS by year.

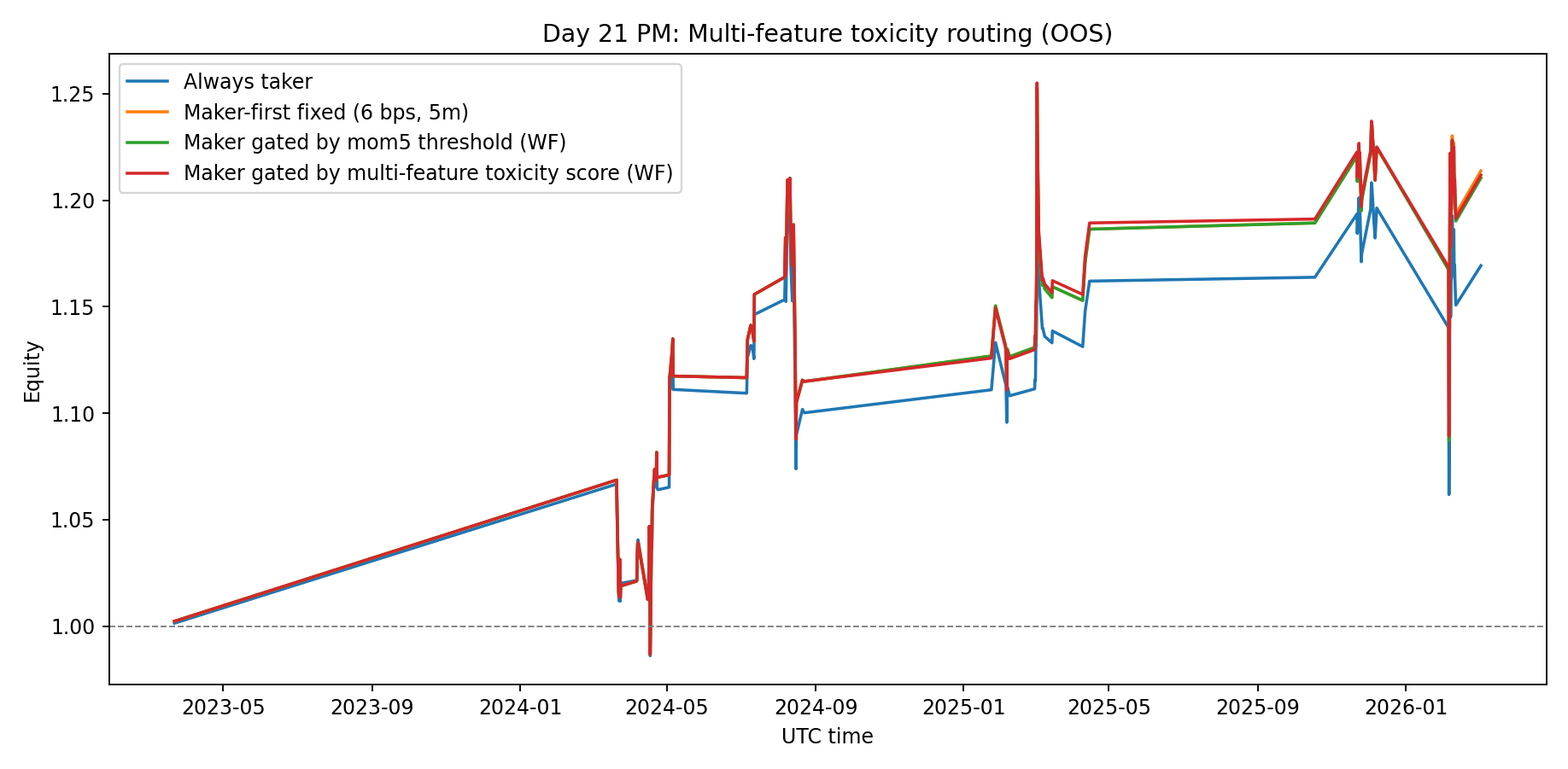

OOS result: still below fixed maker-first

| Strategy | Avg bps/trade | Final equity | 95% stationary-bootstrap CI (bps/trade) | P(mean > 0) |

|---|---|---|---|---|

| Always taker | +15.28 | 1.169x | [-12.25, +43.23] | 86.8% |

| Maker-first fixed | +18.44 | 1.214x | [-9.81, +45.14] | 90.6% |

| Maker gated (mom5 threshold, WF) | +18.22 | 1.210x | [-11.29, +46.37] | 89.6% |

| Maker gated (multi-feature score, WF) | +18.30 | 1.212x | [-9.76, +45.77] | 89.4% |

Key point: multi-feature beats mom5-only by a hair, but is still ~0.14 bps/trade below fixed maker-first.

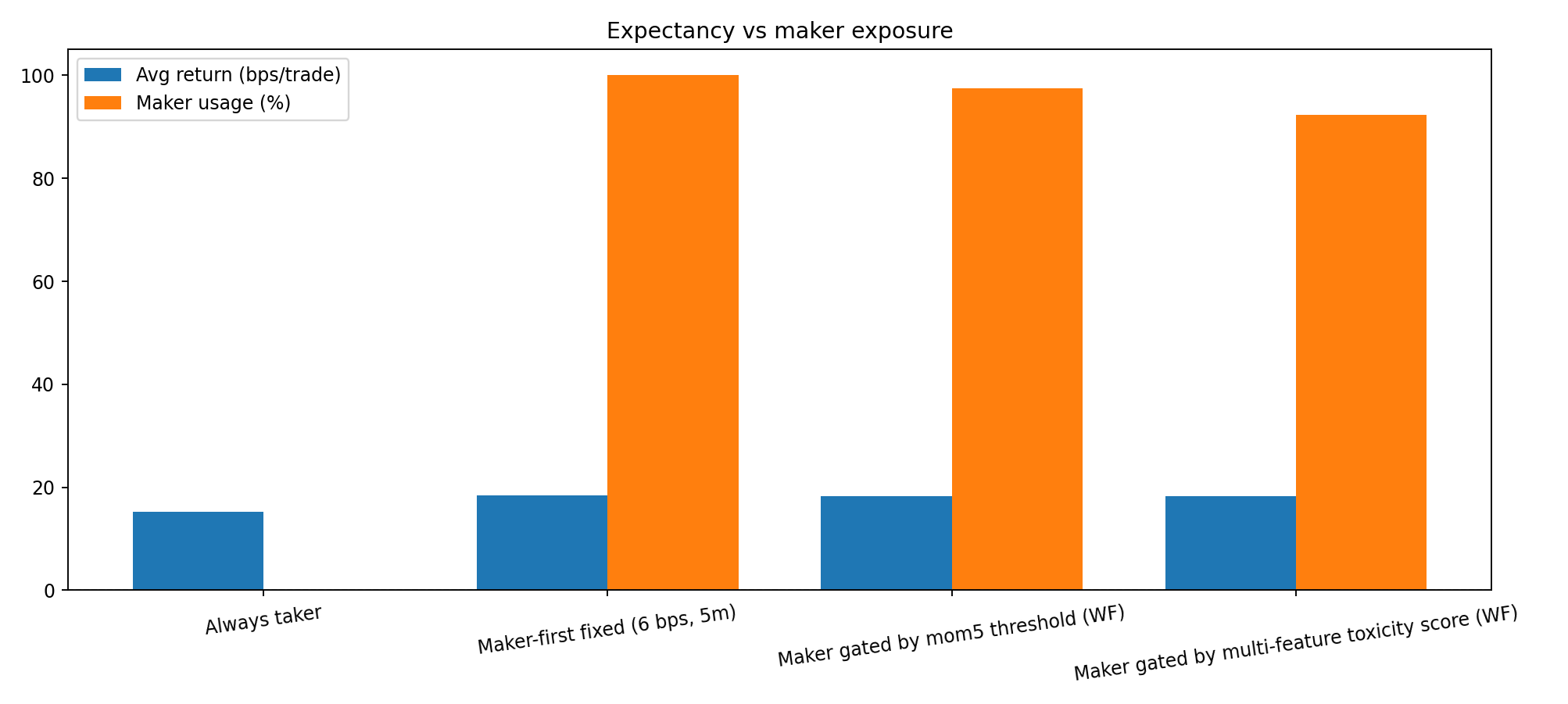

What improved (and what didn’t)

- Maker usage dropped from 100% → 92.4%.

- So the score did route away from some expected-toxic states.

- But the removed trades were not bad enough to create net alpha vs just staying maker.

Same story as AM, just slightly cleaner selection logic.

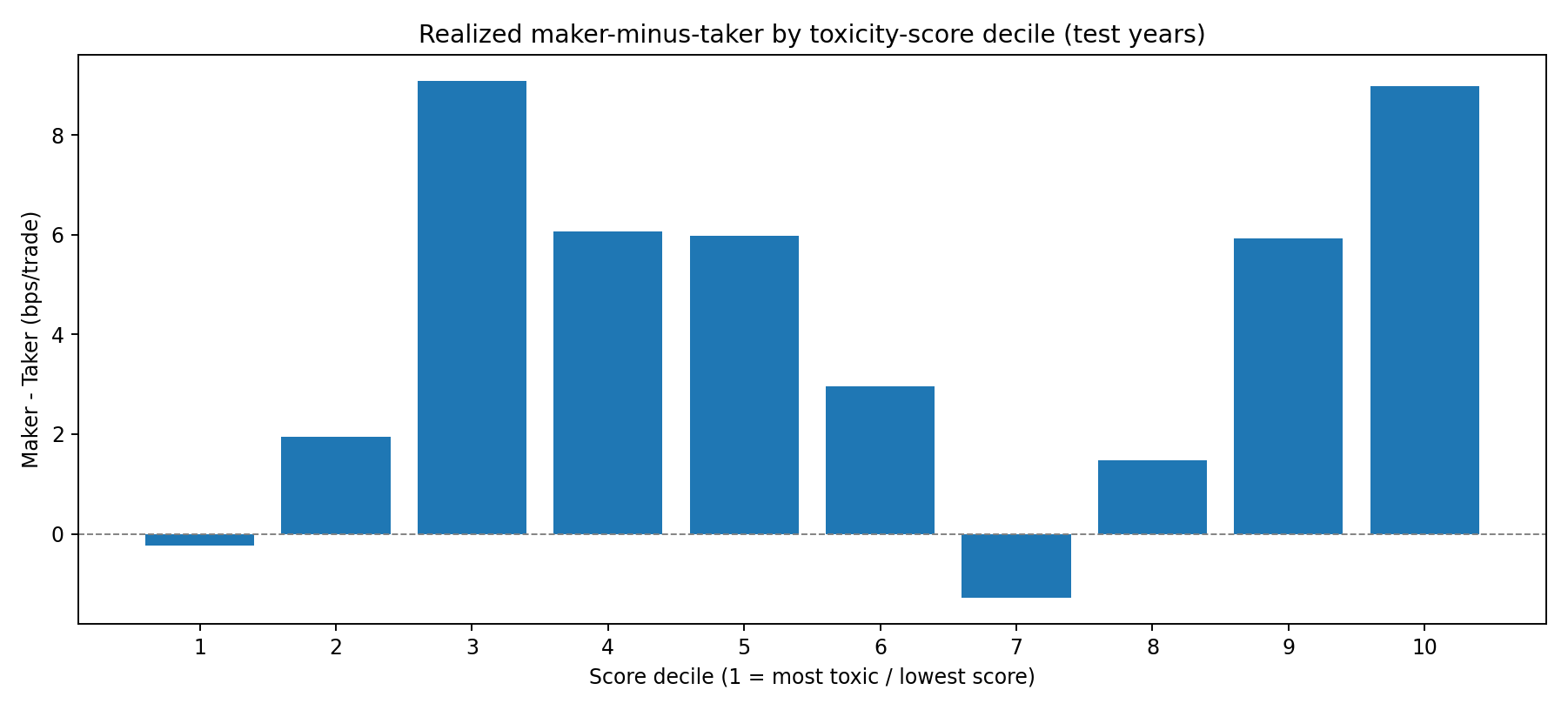

Is the score random? Not fully.

On years where score training was active (2025–2026), realized maker-minus-taker generally improves in higher score deciles, but it’s noisy and non-monotone.

So there is some informational content, but not strong enough for robust routing edge yet.

Honest take

- This is a useful model iteration, not a deployment upgrade.

- Multi-feature routing did not clear the simplest benchmark: fixed 6 bps maker-first.

- All confidence intervals still cross zero.

So: research-only, not deployable.

Reproducibility

Files in this folder:

analyze_multifeature_toxicity_routing.pyday21-pm-multifeature-results.jsonday21-pm-multifeature-equity.pngday21-pm-multifeature-bars.pngday21-pm-score-decile-edge.png

Run:

python3 blog/posts/2026-03-06-multifeature-toxicity-routing/analyze_multifeature_toxicity_routing.pyNext step

Shift from hand-built additive score to probabilistic toxicity modeling with calibrated uncertainty (still walk-forward):

- Predict ((_{maker-taker}>0 x_t)), not just rank score.

- Route maker only when expected edge exceeds a minimum margin after costs.

- Re-run exact same yearly OOS protocol vs fixed maker baseline.

If that still fails, routing is likely second-order; quote geometry and fill mechanics remain first-order.

References

- Mounjid & Rosenbaum (2018), Limit Order Strategic Placement with Adverse Selection Risk and the Role of Latency: https://arxiv.org/abs/1610.00261

- Politis & Romano (1994), The Stationary Bootstrap: https://www.tandfonline.com/doi/abs/10.1080/01621459.1994.10476870

- Avellaneda & Stoikov (2008), High-frequency trading in a limit order book: https://www.researchgate.net/publication/24086205_High-frequency_trading_in_a_limit_order_book

Research only. Not financial advice.